Top Worldpay alternatives for vertical software platforms: Compare embedded payment solutions

May 15, 2026

Blog

Vertical SaaS platforms don't switch from legacy providers like Worldpay because they're outdated. They switch because the model wasn't built for them.

The most common reasons platforms move on:

- Poor commercial terms that compress margins and hide true cost

- Outsourced, slow customer support

- No ownership of merchant relationships or payments data

- No expertise in their vertical, which means generic answers to industry-specific problems

- Limited ability to scale payments revenue inside the product

Worldpay processes a massive volume and has been a payments leader for decades. But its platform is the result of years of acquisitions and legacy infrastructure, not a system designed for embedded payments. For SaaS companies, that creates friction: slow merchant onboarding, limited embedded payment options, poor support, confusing reporting, and fragmented APIs that slow down launches and reduce adoption.

The impact is immediate. Less control over pricing, merchant data, and the payment experience leads to missed volume and compressed margins. Instead of streamlining payment processing, teams end up managing integrations and working around constraints.

This guide breaks down modern Worldpay alternatives purpose-built for vertical SaaS so you can process more volume at higher margins while keeping full control of your payments strategy.

Why vertical SaaS companies are moving away from Worldpay

Worldpay is built around direct merchant relationships, not platform-first experiences. For vertical SaaS companies, that creates a mismatch. You need embedded payment components, white-labeled onboarding, and in-product reporting. Instead, you get payment flows designed for standalone businesses, which limits adoption and reduces control over your merchant data and payment experience.

Integration adds more friction. Worldpay often requires separate APIs for card payments, ACH, digital wallets, and reporting. Each comes with its own certification process, which extends time-to-market and slows new-feature launches. For SaaS teams, that means more engineering effort and delayed revenue from payment processing.

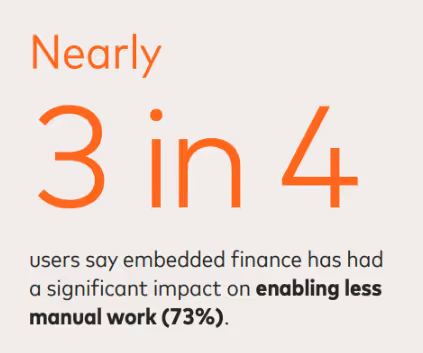

And the cost of that friction is measurable. Research from Mastercard shows that embedded finance reduces manual work by 73% while improving accuracy and reliability by the same margin. Platforms relying on fragmented systems miss these efficiency gains.

Switching can feel risky with multi-year contracts, early termination fees, and limited data portability, all of which create lock-in. But staying is the bigger risk. The future of vertical software is layering fintech products on top of payments—accounting, payroll, banking, lending—and none of that works without owning your payments data and merchant experience. It's also vertical software's moat against AI: platforms that own the data and the relationship stay defensible. The rest get commoditized.

These limitations directly affect core SaaS metrics. Slower onboarding reduces merchant adoption. Poor user experience lowers payment volume. Limited pricing control restricts revenue growth. Over time, the platform absorbs the complexity while the payment provider captures the upside.

Top Worldpay alternatives for vertical SaaS payment processing

Choosing the right payment provider directly impacts your revenue, adoption, and time to market. For vertical SaaS platforms, you need to do more than simply process online payments. You need to embed payments into your product, streamline onboarding, and capture more value from every transaction.

The best Worldpay alternatives offer all-in-one payment processing solutions with support for credit cards, ACH, digital wallets like Apple Pay and Venmo, and recurring billing through a single API. They also give you more control over pricing, merchant accounts, and the full payment experience.

Here’s how the leading payments platforms compare.

Rainforest: purpose-built for vSaaS

Rainforest is purpose-built for vertical SaaS platforms that want to act like a payment facilitator by owning the merchant relationship, the data, and the revenue without the compliance overhead of actually becoming one. It's a PayFac-lite model: fully embedded, fully white-labeled, with Rainforest handling PCI, underwriting, and fraud behind the scenes. Your merchants never interact with Rainforest. You own the experience end-to-end.

Key strengths:

- One integration, one API for card payments, ACH, digital wallets, PayPal (including Venmo and PayPal Pay Later), and point-of-sale

- Fully white-labeled merchant onboarding, underwriting, and payment experience

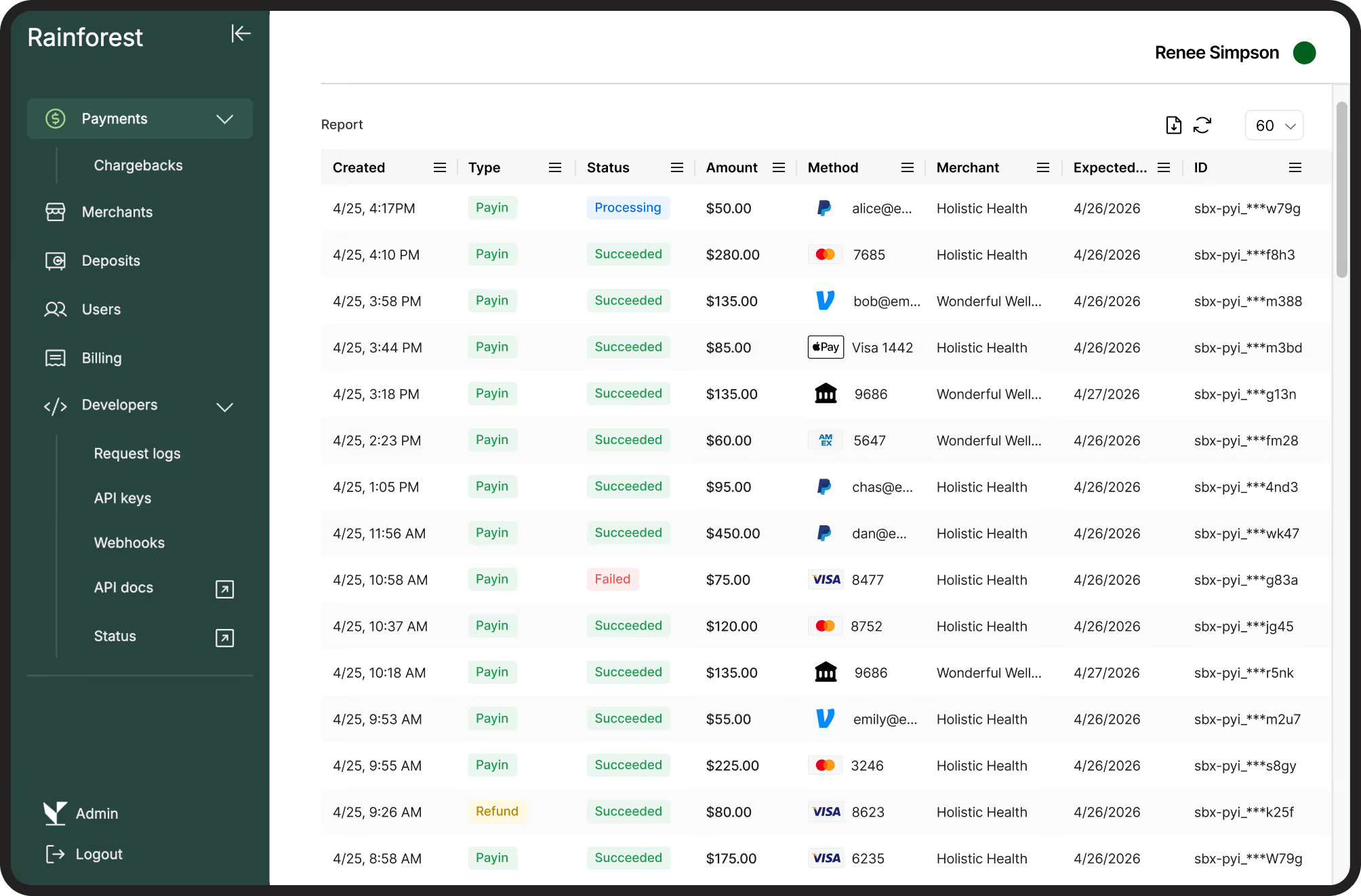

- Transparent, penny-perfect reporting down to the transaction level

- Built-in compliance, fraud prevention, and chargeback management

- Rainforest absorbs losses due to risk

- Strategic program management with real human customer support

- Guarantees full ownership and portability of payments data

Best suited for:

- Vertical software platforms looking for purpose-built solutions and a partner to scale their payments volume into the billions.

Trade-offs:

Currently optimized for U.S. card volume. International expansion is on the roadmap and is worth a direct conversation if cross-border processing is a near-term requirement.

Stripe Connect: for multi-tenant SaaS platforms

Stripe Connect is a developer-first payments platform with mature tooling for multi-tenant environments.

Key strengths:

- Fast deployment with sandbox access in minutes and go-live in days to weeks

- Programmatic sub-merchant account creation via Connected Accounts

- Built-in support for splitting payments across multiple parties

- Proven scalability powering platforms like Shopify, DoorDash, and Spotify

Best suited for:

- Developers looking to launch payments as quickly as possible, knowing they will eventually outgrow the solution.

Trade-offs:

Stripe defaults to its own branding, limiting full white-label control, and locks you into a single processor, reducing pricing leverage as you scale. Hidden fees add up fast. Radar charges per-transaction fraud fees, and Stripe doesn't refund interchange on refunded transactions, so margin disappears on every reversal. Support runs through third-party vendors, which slows resolution when issues come up.

Adyen: for Platforms SaaS solutions

Adyen provides enterprise-grade payment service for platforms operating at global scale.

Key strengths:

- Single API across online payments, in-app, and POS

- Interchange++ pricing with detailed cost visibility

- Support for cross-border payments and local payment methods

- Advanced capabilities like custom splits and settlement controls

Best suited for:

- Platforms processing multiple billions in volume annually, with very complex payment flows and need international support.

Trade-offs:

Longer onboarding timelines and complex contract negotiations can delay launches, especially for earlier-stage platforms.

PayPal Commerce Platform for rapid integration

PayPal Commerce Platform offers quick access to a global payments platform with pre-built components.

Key strengths:

- Pre-built checkout experiences that reduce front-end development

- Supports 200+ markets and 25+ currencies

- Split payout functionality for multi-tenant platforms

- Built-in support for PayPal, Venmo, and digital wallets

Best suited for:

- Platforms that want fast deployment with global payment method coverage and don't require full white-label branding control.

Trade-offs:

PayPal branding remains in the checkout experience. Pricing lacks transparency and requires custom negotiation, making margin optimization harder.

Payabli for complex payment operations

Payabli is designed for platforms managing complex payment flows and hierarchical merchant structures.

Key strengths:

- PayFac-as-a-Service model with automated KYB and KYC

- Native split payments and flexible fund distribution

- Strong support for complex pricing and merchant hierarchies

Best suited for:

- Platforms with majority high ticket ACH payments.

Trade-offs:

Pricing isn't publicly available, which slows evaluation and planning. Payouts run through third parties, onboarding tends to be slow, and as a newer company, scale is still limited.

Essential payment features for vertical SaaS platforms

Generic payment gateways force you to build everything yourself. Purpose-built platforms handle these layers natively, letting you launch faster and capture more revenue per transaction. As you evaluate options, focus on capabilities that support embedded payments, multi-tenant architecture, and program-level control.

Multi-tenant payment architecture

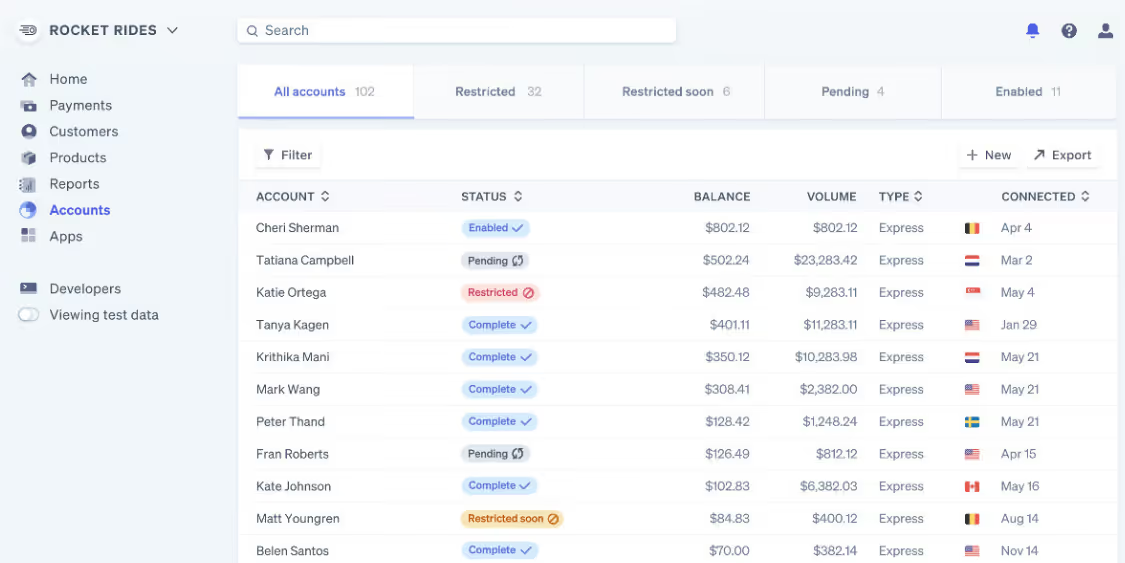

Your platform needs infrastructure that supports independent merchant accounts under a single master relationship. Multi-tenant architecture lets each customer process payments with their own merchant ID, settlement schedule, and pricing while you maintain full control over program economics and merchant data.

Without it, all transactions sit under a single merchant account. That limits pricing flexibility, creates compliance risk, and makes scaling onboarding difficult without manual work.

Look for providers that support:

- Programmatic sub-merchant creation via API

- Hierarchical fund splitting

- Tenant-level reporting with platform-defined metadata

Rainforest delivers all three with embedded merchant onboarding and in-context reporting that keeps the entire experience in your platform, without redirects or third-party branding.

Vertical-specific risk & compliance requirements

Every vertical comes with its own risk profile and regulatory requirements. Healthcare platforms face HIPAA constraints and high-dollar transaction monitoring. Home services platforms need contractor verification and flexible volume handling. A payments provider built for generic ecommerce won't understand these nuances.

Rainforest acts as a strategic program manager, working with your team to configure underwriting and risk thresholds that balance risk and compliance with user experience. You get vertical-specific expertise from real humans who understand your business model, which means faster onboarding, fewer merchant drop-offs, and higher payment margins without sacrificing compliance or security.

Want to see these features in action? Book a demo.

How to evaluate and migrate from Worldpay to a new provider

Switching from Worldpay requires careful planning across technical integration, merchant data migration, and revenue impact. The right approach makes the transition easy, minimizes disruption, and maximizes long-term profitability.

Technical migration and integration planning

Start by auditing your current Worldpay integration points, including every API call, webhook, and data dependency your payment system relies on. Request sandbox access from shortlisted providers early so your engineering team can test parallel integrations before committing.

- API parity and feature mapping: Confirm your new provider supports all payment methods and transaction types you currently process, including card-present, ACH, and digital wallets like Apple Pay and Venmo.

- Data migration requirements: Plan how you'll transfer merchant accounts, transaction history, tokenized payment methods, and linked bank accounts.

- Parallel processing windows: Run dual integrations for 30–60 days to validate transaction accuracy, reconciliation, and cashflow before full cutover

- PCI and compliance continuity: Ensure your new integration maintains PCI DSS compliance and built-in fraud prevention without requiring re-certification

Rainforest simplifies migration with a single API consolidating card processing, ACH, and popular wallets. Expect a technical migration timeline of 4–12 weeks, depending on your platform's complexity. Providers with clear migration documentation and responsive human support can significantly compress this.

Financial impact and cost analysis

Switching providers is a revenue decision, not just a technical one.

Start with your current costs:

- Pull the last 6 months of processing statements

- Calculate your effective rate per transaction

- Include all fees: interchange, assessments, gateway, and monthly minimums

Many vertical SaaS platforms find they are overpaying after auditing their Worldpay contracts line by line.

Evaluate pricing models:

- Interchange-plus pricing typically delivers better margins

- Blended or tiered pricing can hide true costs

- Margin improvements compound as your transaction volume scales

Plan for migration costs:

- Engineering time for integration

- Parallel processing during transition

- Merchant communication and onboarding

Often, platforms see positive ROI within 3 to 6 months when moving to a provider with transparent pricing, better payment options, and embedded revenue-sharing.

FAQs about Worldpay alternatives

What are the main disadvantages of using Worldpay for vertical SaaS companies?

Worldpay’s main drawbacks include limited embedded payment components, complex integrations, and rigid contract terms that slow time-to-market. While it supports recurring billing, it isn’t designed as a full subscription management layer for SaaS platforms. Workflows like subscription lifecycle management, automated onboarding, and in-platform reporting often require additional tools or custom development.

As a result, teams lose control over merchant data, pricing, and the overall payment experience, making it harder to improve adoption, streamline operations, and scale payments revenue efficiently.

How long does it typically take to migrate from Worldpay to an alternative payment provider?

Migration timelines typically range from 4–12 weeks, depending on your platform's technical complexity, merchant volume, and the new provider's onboarding process. Purpose-built providers can accelerate this by offering embedded onboarding, built-in automation, and simplified integrations. The timeline includes API integration work, data migration planning, merchant re-onboarding, parallel testing, and phased rollout. Working with a provider that offers dedicated migration support and vertical-specific expertise accelerates the process and reduces risk to existing merchant relationships.

Which Worldpay alternative offers the best partnership for long-term growth?

Rainforest offers the strongest partnership for long-term growth because it's purpose-built for vertical SaaS platforms that want to own their payment experience and maximize revenue.

Unlike generic payment providers, Rainforest delivers fully embedded, white-labeled payments with transparent transaction-level profitability reporting and a single integration covering all payment methods. The platform's strategic program management approach means you work with real human experts who understand your vertical.

Choose the right payment strategy for your vertical SaaS

Your payment strategy directly impacts adoption, volume, and long-term revenue.

The right Worldpay alternative should align with your vertical, growth timeline, and ability to own the merchant experience without adding operational overhead.

Prioritize providers with transparent, interchange-plus pricing so you can see exactly what you earn on every transaction. Blended rates hide margins and make forecasting harder as you scale. Instead, look for a payments platform with developer-friendly APIs, embedded components, and support for credit cards, ACH, digital wallets like Apple Pay and Venmo, and recurring billing through a single integration.

Rainforest is purpose-built for vertical SaaS platforms that want full control of their payment processing strategy. With one integration and one API, you get fully embedded, white-labeled payments without added complexity. It handles compliance, risk, and underwriting, with an expert team that provides hands-on support to help you drive adoption and grow volume.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc