Stripe Connect alternatives for vertical software platforms: Compare embedded payments software

May 14, 2026

Blog

Stripe built a powerful payments processing platform for online businesses, but it wasn’t designed for vertical SaaS platforms that need to embed payments, control merchant relationships, and generate revenue from their customers’ online payments. While Stripe Connect is their answer to this problem, the solution feels like it’s trying to fit a square peg in a round hole.

Although quick and easy to get started, as platforms scale payments on Stripe Connect, the shortcomings become obvious, and platforms ultimately realize they’re leaving money on the table. There are Stripe Connect alternatives for vertical SaaS that better align with their business model, merchant experience, and long-term economic goals.

This guide compares purpose-built payment platforms that help vertical SaaS companies earn revenue when their customers get paid, while maintaining full control over merchant relationships, data, and the entire payments lifecycle.

Why SaaS companies are exploring Stripe Connect alternatives

Vertical SaaS companies have a fundamentally different relationship with payment processing than standalone merchants. You’re not just accepting online payments. You’re onboarding merchants, managing their checkout experience, and supporting transactions across the full payments lifecycle.

Generic providers like Stripe weren’t designed for that model. As your transaction volume grows, that mismatch shows up in your margins through processing fees, limited pricing control, and missed revenue opportunities. The economics make it obvious: platforms using purpose-built embedded payments solutions report 3–4x higher revenue per customer than those relying on generic processors. That delta doesn't come from processing more volume–it comes from actually owning the revenue your merchants generate.

Beyond pricing, the operational burden compounds quickly. Managing fragmented integrations, reconciling data across systems, and handling merchant support for a payment platform you don’t fully control creates constant friction. Instead of improving your product, your team is stuck troubleshooting someone else’s infrastructure.

The true cost of Stripe Connect’s one-size-fits-all approach

Stripe's horizontal model creates real margin pressure for vertical SaaS companies. You pay the same transaction fees and processing fees as a standalone merchant, even though you manage merchant acquisition, onboarding, and support.

The same one-size-fits-all approach shows up in risk. Stripe treats every platform identically, regardless of vertical. Payments for HVAC contractors look nothing like payments for doctors' offices, but Stripe's risk thresholds don't reflect that. The result is constant holds and merchant friction long after onboarding is complete. Rainforest takes a platform-level view of risk that matches how each vertical actually transacts, so once a merchant is onboarded, they're fully onboarded.

Support follows the same pattern. A partner that understands vertical SaaS spots opportunities a generic processor misses, like interchange optimization, which Stripe rarely surfaces and rarely tunes for individual platforms.

The real cost goes beyond pricing. It shows up in time spent working around limitations, trying to decipher residual reports that don't line up, and increased churn when merchants face friction during online payments. You also miss out on revenue you could capture through pricing control, routing optimization, and deeper visibility into your payments lifecycle.

Over time, what looks like a simple payment solution becomes a constraint. You absorb the complexity, while the provider captures the upside.

Built for vertical SaaS, not bolted on. Book a demo.

Top Stripe Connect alternatives for SaaS businesses to consider

The right embedded payments solution should do more than process transactions. It should let you monetize payment processing, control the full checkout experience, and manage the entire payments lifecycle from onboarding to payouts.

For vertical SaaS companies, that means choosing an all-in-one payment solution that supports online payments, scales with your transaction volume, and keeps everything in-platform.

Here’s how the best Stripe alternatives compare.

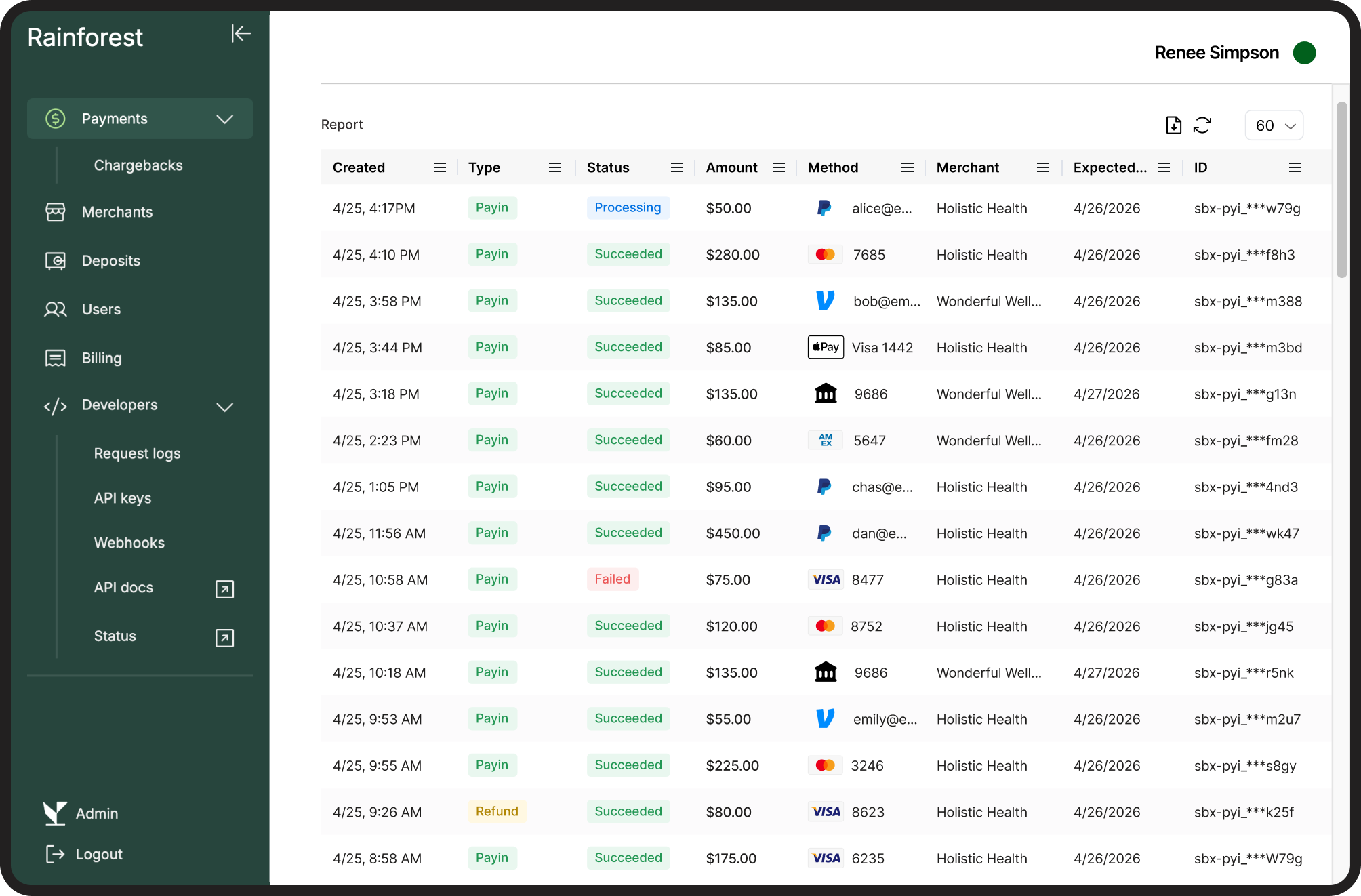

Rainforest (purpose-built for vertical SaaS)

Rainforest is the only embedded payments platform purpose-built for vertical SaaS platforms—not adapted from an ecommerce product, not bolted onto a generic acquiring stack. The model is PayFac-as-a-service: you act like a payment facilitator, owning the merchant relationship and capturing the revenue, without taking on the compliance overhead of actually becoming one.

Rainforest handles PCI, underwriting, fraud, and chargebacks. Your merchants onboard through your interface, process under your brand, and never interact with Rainforest. You own the experience and the economics end-to-end.

With a single, developer-friendly API, you can support credit cards, debit cards, ACH, PayPal, Venmo, and PayPal Pay Later, without managing separate integrations or disrupting your checkout experience.

Best for: Vertical SaaS platforms that want to own payments. If your goal is to turn payment processing into a revenue line, control the merchant relationship, and avoid building your own compliance infrastructure, this is the platform.

Key features:

- White-labeled onboarding and in-platform payment processing. Merchants never see Rainforest

- Interchange-plus pricing with full transaction-level visibility—you see exactly what you earn on every payment

- Real-time dashboard with transaction-level profitability reporting vs. blended summaries, actual margin per transaction

- Built-in fraud protection, compliance, and risk management. Rainforest owns risk. No need to hire and manage a dedicated risk team

- All-in-one infrastructure for managing the full payments lifecycle

- Dedicated human support and strategic program management. A real team that knows your vertical, not a ticket queue

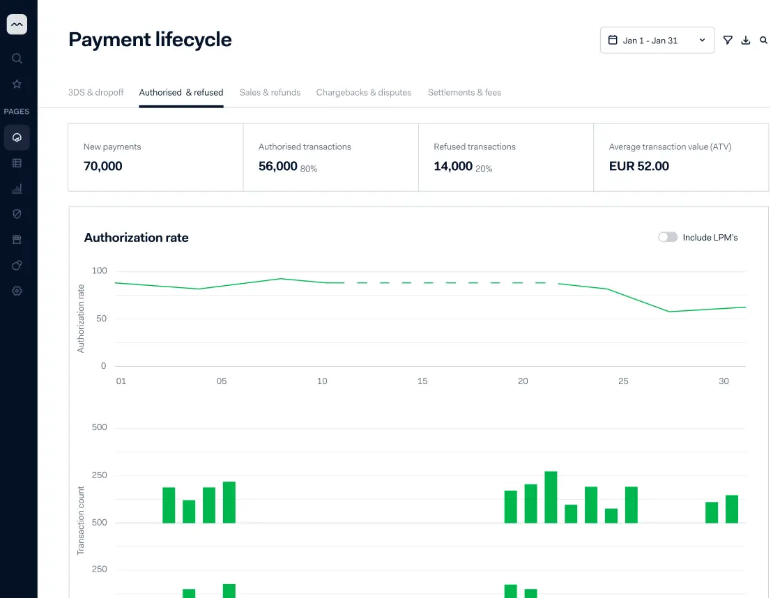

Adyen (enterprise, global scale)

Adyen is a global payment service provider with strong support for international payments and enterprise-scale operations. Its unified platform handles payments, risk, and settlement through a single API, with advanced optimization for authorization rates.

Best for: Large SaaS platforms with global requirements and the resources to support complex implementations.

Key features:

- Broad support for global payment methods and multi-currency transactions

- Built-in fraud protection and risk tools

- Direct acquiring to optimize authorization and reduce failed transactions

- Unified API across payments, risk, and settlement

- Designed for high transaction volume and enterprise scalability

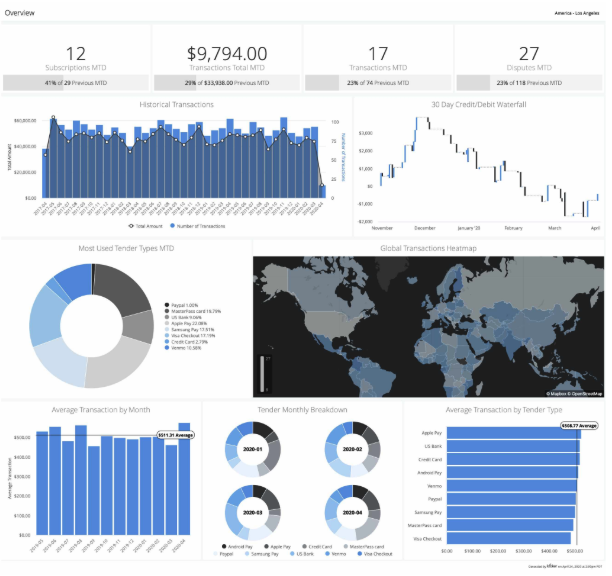

Braintree (PayPal ecosystem integration)

Braintree, part of PayPal, is a payment gateway and processor that combines card processing with native PayPal and Venmo support. It’s known for being developer-friendly and supporting recurring payments and subscription models.

Best for: Mid-market SaaS platforms that want PayPal and Venmo integration without managing separate relationships

Key features:

- Native PayPal and Venmo integration for flexible payment options

- Support for recurring payments and subscription management

- Marketplace functionality with split payments

- Multi-currency support for international payments

- Flexible APIs for customizing the checkout experience

Finix (build-your-own payments program)

Finix provides payment infrastructure for platforms that want to build and operate their own payments program. You control pricing, onboarding, and merchant accounts, while Finix handles compliance, risk, and sponsor bank relationships.

Best for: SaaS platforms ready to invest in becoming a Payfac themselves with dedicated internal resources.

Key features:

- Full control over merchant onboarding and pricing models

- PayFac infrastructure with compliance, underwriting, and fraud protection

- Customizable payment flows and routing logic

- Support for scaling transaction volume over time

- Designed for teams managing payments as a core product function

How to choose the best payments provider for your SaaS platform

This is one of the most important decisions a vertical SaaS platform will make. At maturity, payments can account for more than 50% of platform revenue. The payments data also powers the next wave of embedded fintech offerings like accounting, banking, and lending. And once payments are embedded into your product, your platform becomes genuinely sticky in a way that pure software rarely is.

Getting this right early compounds for years. Getting it wrong forces years of unwinding a provider relationship that caps your margin, your data, and your ability to expand.

Evaluating Stripe Connect alternatives comes down to three core areas. Pricing transparency, partner support, and control over your merchant relationships. The right payments platform should align with your platform economics, not force you into a generic payment processing model that leaves revenue on the table.

The best providers don't just offer infrastructure. They act as a true partner. That means responsive, human customer support, deep expertise in your vertical, and a shared focus on helping you scale your transaction volume without adding operational complexity.

Analyzing pricing structures and hidden fees

Pricing transparency separates providers built for platform economics from those designed to maximize their own margin. You need to understand the full fee structure, not just the headline rate or advertised transaction fees.

Common pricing models include:

- Interchange-plus: actual network cost plus a fixed markup, giving you clear visibility into margin

- Flat-rate (blended): one rate for all transactions, often hiding higher costs on premium cards

- Tiered pricing: transactions grouped into buckets, making true cost difficult to predict

Beyond transaction rates, watch for fees that erode revenue:

- Monthly fees

- Per-merchant account fees

- Radar fees

- Not refunding interchange on returns

- PCI compliance fees

- Chargeback fees

- Early termination penalties

Some providers also require a share of your payment revenue, limiting your upside as you scale.

Transparent pricing makes revenue predictable. The best providers for vertical SaaS offer interchange-plus pricing, no mandatory revenue share, and flexible contract terms.

Evaluating integration requirements and API quality

Your integration timeline depends on how the provider structures their API and documentation. Look for a single integration point, not multiple SDKs, separate onboarding flows, and disconnected systems.

Evaluate these areas:

- Single API coverage for cards, ACH, alternative methods, onboarding, KYC, and reporting

- Clear documentation with vertical-specific examples

- Reliable webhooks with strong error handling for real-time updates

- Sandbox environments that mirror production behavior

- White-label flexibility to keep the entire checkout experience and onboarding flow in-platform

Purpose-built platforms for vertical SaaS typically launch faster because they solve these challenges upfront. Generic providers often require custom development to achieve the same level of control, extending your time to revenue.

Ensuring compliance and robust security standards

Compliance and security are foundational when handling payments at scale. Your provider should manage PCI DSS Level 1 certification, KYC and AML screening, and real-time fraud monitoring, so you do not need to build or maintain this infrastructure yourself.

Look for:

- Automated KYC and AML workflows during merchant onboarding

- Real-time fraud protection and configurable risk controls

- Chargeback management tools with built-in evidence workflows

- Audit trails for reporting and regulatory visibility

The best embedded payments providers treat compliance as a core service. They monitor regulatory changes and update their systems proactively, so your platform stays protected as you scale.

Key considerations when switching from Stripe

Switching payment providers affects your revenue, merchant relationships, and platform stability. You need a migration plan that doesn’t disrupt your existing transaction volume while setting up a more profitable model long-term.

Planning for data migration and customer impact

Start by auditing the data you need to migrate. That includes payment history, transaction records, merchant onboarding details, and settlement data. Map everything to your new provider’s data model, and prioritize providers that offer structured access to historical data to avoid manual work.

Set clear expectations with your merchants. Communicate timelines, what’s changing, and what stays the same. If you’re moving to a white-labeled solution, reinforce that the checkout experience and payments flow remain fully in-platform.

Reduce risk with a phased rollout. Route new merchants to the new provider first, while existing merchants stay on Stripe. Migrate your highest-volume merchants last, after validating onboarding, payouts, and reporting.

Developing testing and rollback strategies

Before switching, create a controlled testing environment. Run both providers in parallel and route a small percentage of payment processing through the new system while keeping Stripe as a fallback.

Focus testing on:

- End-to-end transaction processing across all payment methods

- Merchant onboarding and KYC flows

- Reconciliation and reporting accuracy

- Webhook reliability and error handling

Define rollback triggers in advance, such as error rates or settlement delays. Document how to revert systems and communicate changes if needed.

Providers with dedicated migration support simplify this process and help you move to full deployment faster.

Frequently asked questions about Stripe alternatives

What is the cheapest alternative to Stripe for SaaS?

The cheapest Stripe alternative for SaaS isn’t always the most cost-effective. Lower transaction fees often come with limited control over payment processing and fewer revenue opportunities.

Purpose-built platforms using interchange-plus pricing let you add your own markup and capture more margin. When evaluating cost, consider total economics, including margin potential, integration effort, and support, not just transaction rates.

Can I use multiple payment processors simultaneously?

Yes, but managing multiple payment processors adds complexity. You’ll need to handle split reconciliation, duplicated compliance workflows, and fragmented support across systems.

Most vertical SaaS companies simplify by using a single payment platform that supports multiple payment methods through one integration. If you need multiple providers to fill gaps, it’s usually a sign your current solution isn’t meeting your needs.

How long does it take to switch from Stripe to another processor?

Most vertical SaaS companies can switch payment processing providers in 4 to 12 weeks. Timelines depend on platform complexity, data migration, and testing requirements.

Purpose-built providers with structured migration support can accelerate onboarding and reduce risk. Generic processors often take longer due to fragmented integrations and manual steps, which can delay time to revenue.

Start earning revenue from your platform's payments

Generic payment providers leave money on the table. When you rely on solutions built for ecommerce, you miss the core advantage of embedded payments for vertical SaaS: earning revenue when your customers get paid.

Purpose-built providers give you control and upside. You keep the merchant relationship, launch faster with a single API across payment methods, and gain visibility into transaction-level economics. They also handle compliance, risk, and support so you can focus on growing your platform.

Rainforest is your strategic program manager for embedded payments. We help you process more volume at higher margins while handling compliance, fraud monitoring, and PCI.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2025 Rainforest Pay, Inc