Embedded payments software for vertical SaaS: How to turn payments into revenue

May 8, 2026

Blog

Every payment your customers process generates transaction fees. For many vertical software platforms, that revenue goes to third-party payment providers, along with the merchant relationship, the data, and any shot at owning that revenue long-term.

You also take on hidden risk. Fraud, chargebacks, and compliance sit outside your control.

Embedded payments software shifts payments from a cost center to a direct profit driver while keeping every part of the merchant experience within your platform. This guide breaks down how embedded payments software works and how to find the right fit for your organization.

What is embedded payments software for vertical SaaS platforms?

Embedded payments software is white-labeled payments infrastructure that allows vertical SaaS platforms’ merchants to accept payments directly within the platform. This lets vertical SaaS platforms act like a payment facilitator (payfac as a service)—owning merchant onboarding, processing, and revenue—without building the compliance infrastructure of an actual PayFac. The right partner handles PCI, underwriting, and fraud. You get the economics and the relationship.

This differs fundamentally from traditional payment integrations. When you rely on external payment processors or redirect merchants to a third-party checkout, you lose control of the customer experience, the merchant relationship, and revenue opportunity.

With embedded payment software, all payment workflows stay inside your platform. Your customers onboard through your interface, process transactions under your brand, and treat your platform as their single source of truth for payment data. You control the experience, streamline operations, and capture the full economics.

How embedded payments software works within vertical SaaS ecosystems

Embedded payments software sits between your platform and the underlying payment systems that move money.

When a customer makes a payment, the transaction:

- Flows through your branded interface

- Hits the embedded payments platform via API

- Routes through the appropriate network (credit cards, ACH, or wallets)

- Settles funds while maintaining full visibility and control

With Rainforest’s single API, you can support multiple payment methods—including cards, ACH rails, and wallets like PayPal and Venmo—without building separate integrations for each. Merchants onboard through your interface, process under your brand, and never interact with Rainforest directly. You own the relationship end-to-end.

Payment processing integration architecture

The architecture centers on a single API connection that routes payment requests across multiple rails and networks.

.avif)

Core components include:

- An authentication layer that secures API calls with tokenized credentials

- A payment routing engine that directs transactions to the optimal path

- Network connectivity to card networks and ACH rails

- Settlement infrastructure that manages fund movement on your defined schedule

- A webhook system that pushes real-time transaction status updates back to your platform

This approach streamlines and automates payment processing, so you maintain full control over merchant onboarding flows, while Rainforest handles PCI compliance, fraud monitoring, and network certifications.

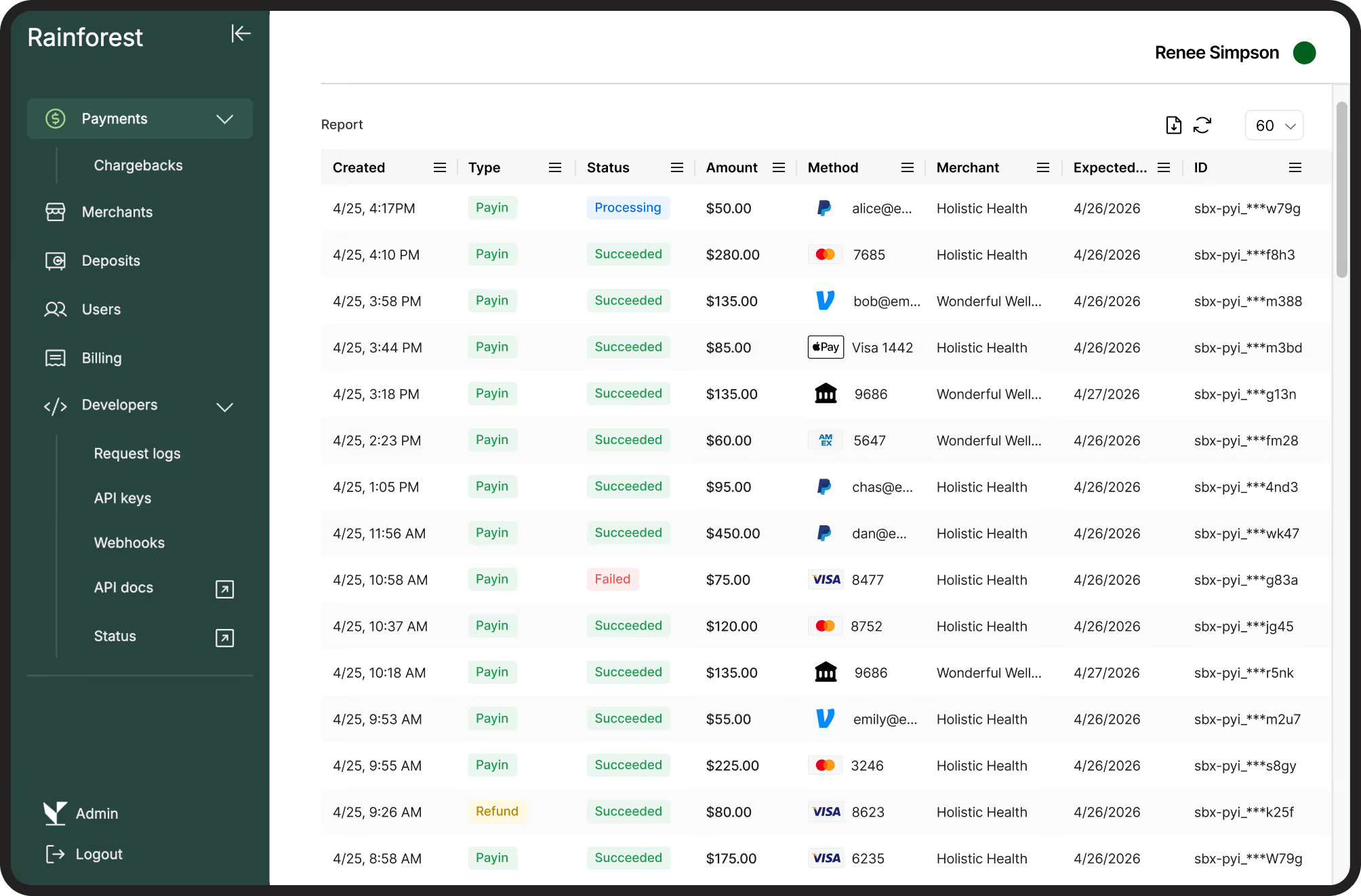

Data flow and transaction management

Your platform sends transaction data through a single API call. The system routes the request, returns an authorization response in real time, and standardizes the data across all payment options.

You receive structured transaction records that include merchant ID, payment method, amount, status, fees, and settlement data, giving you full visibility into your payments technology stack.

Beyond authorization, the platform manages the full lifecycle, including captures, refunds, and chargebacks. Webhooks notify your system of every update, so you can maintain accurate records and deliver a consistent customer experience.

What are the key benefits of embedded payments for vertical SaaS?

Embedded payments software delivers three core advantages that directly impact your bottom line, including new revenue streams, improved customer experience, and operational efficiency.

Revenue generation through payment monetization

When you own your payments stack, you earn margin on every transaction your customers process. Instead of passing that value to third-party providers, you turn payment processing into a scalable revenue stream built directly into your product.

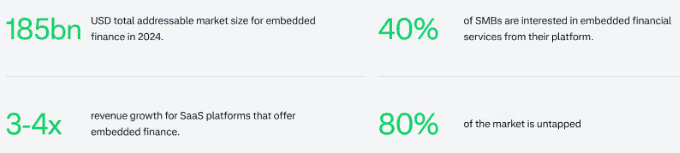

And the impact is significant. According to Adyen’s 2024 Embedded Finance report, SaaS platforms that embed financial services can see 3–4x higher revenue per customer, without needing to build new features or acquire new users.

Many platforms underestimate this opportunity because they lack visibility into which payment methods, use cases, and customers drive margin. That visibility is what separates platforms that treat payments as a feature from those that treat them as a scalable revenue line.

Enhanced customer retention and platform stickiness

Payments create switching costs. When your customers run their entire payment operation through your platform, including onboarding, processing, reporting, and reconciliation, they’re far less likely to churn. You become infrastructure, not just software.

As transaction volume grows, customers build up valuable payment data, stored payment details, and financial records that are tightly integrated into your product. That makes your platform harder to replace and improves long-term customer satisfaction.

You also gain full visibility into transaction patterns and customer health metrics. This allows you to proactively identify risk, improve payment capabilities, and support customers before issues impact retention.

Operational efficiency and reduced payment friction

Embedded payments software eliminates the fragmented experience of third-party integrations. Instead of juggling multiple service providers, your customers manage all online payments inside a single, unified workflow. They don’t get redirected to external systems or reconcile across disconnected tools. This creates a more consistent user experience and reduces friction at every stage of the payment lifecycle.

For your internal teams, this means fewer support tickets, simpler troubleshooting, and unified reporting. Your finance team gets settlement data, transaction fees, refunds, and chargebacks flowing through the same system they already use.

Purpose-built payments technology also helps you automate key processes like KYC, PCI compliance, fraud monitoring, and dispute management—without building your own payment infrastructure.

Rainforest helps vertical SaaS platforms launch embedded payments in days without taking on the compliance load.

How to choose the right embedded payments software for your vertical SaaS platform

For vertical SaaS platforms, choosing the right embedded payments software comes down to three areas: how easily the system integrates into your product, how risk and compliance are managed, and how commercial terms impact your long-term margins.

Technical integration requirements and API capabilities

Your embedded payments solution should fit into your existing tech stack, not force a rebuild. Look for a single API that connects you to multiple payment methods so you don’t have to manage separate integrations.

Strong API capabilities should include:

- Real-time transaction updates via webhooks

- A sandbox environment for testing

- Clear documentation and predictable workflows

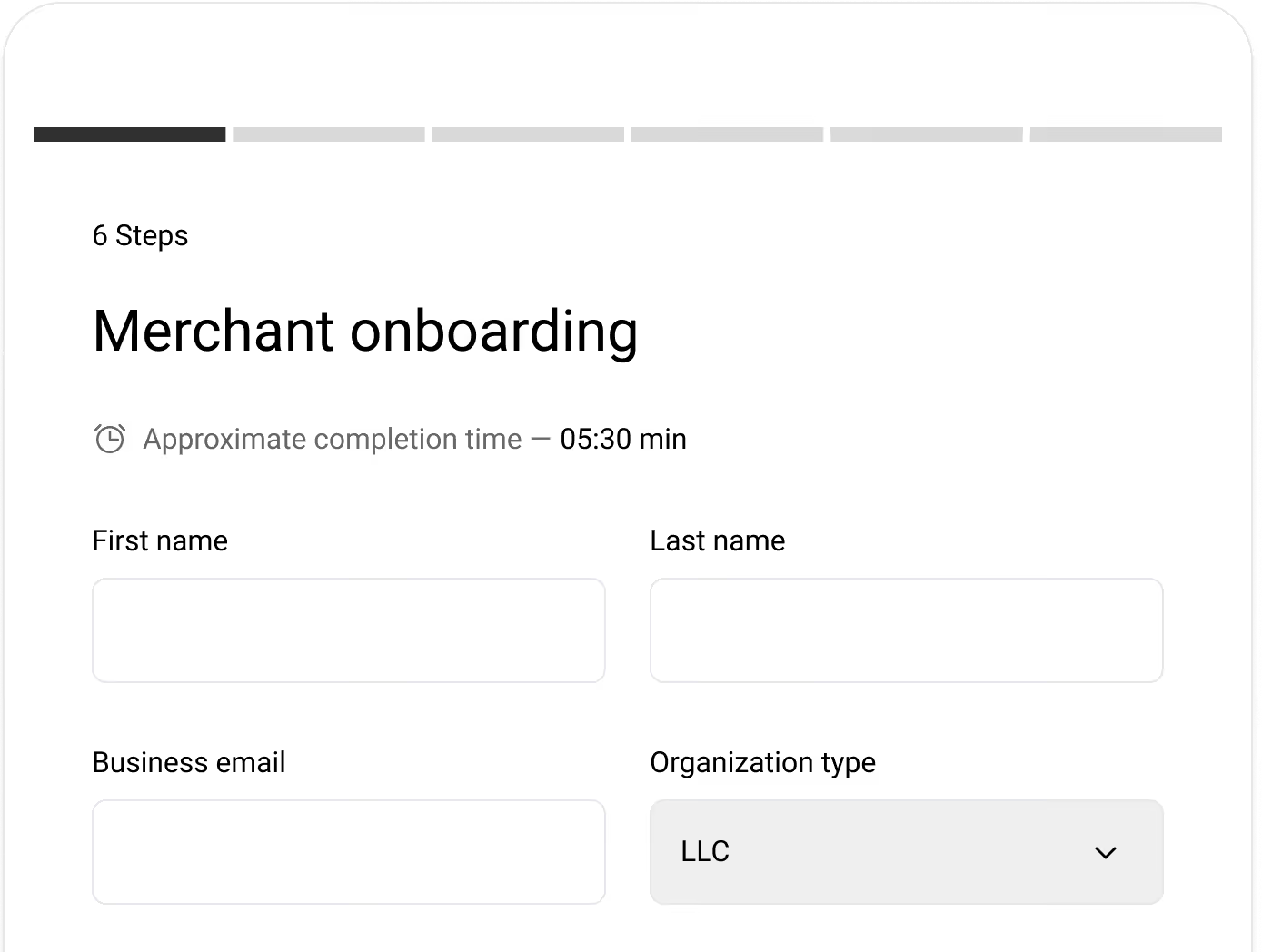

Beyond connectivity, integration should support merchant onboarding and migration at scale. Pre-built, white-labeled onboarding flows and automated KYC checks help you bring customers onto your platform faster and start processing online payments sooner.

You should also have access to granular payment data, including authorization rates, decline reasons, and transaction-level costs, so you can troubleshoot issues and improve payment capabilities over time. If a provider can’t show a working sandbox or a clear implementation path early, it’s a sign that the platform wasn’t built for vertical SaaS.

Compliance and security considerations

Payments introduce regulatory and operational risk. The right provider should handle this for you, not push it back onto your team.

Compliance in embedded payments is complex and getting harder. In fact, Alloy’s 2024 State of Embedded Finance report shows that 80% of organizations involved in embedded finance struggle to manage compliance requirements. The compliance burden is real—but it's a reason to choose the right partner, not a reason to avoid embedded payments.

To avoid these non-compliance issues, look for platforms that manage:

- PCI Level 1 compliance, including tokenization and encryption

- Fraud monitoring and real-time risk detection

- Chargeback handling and dispute workflows

Underwriting should also be flexible. Some payment providers require you to take on full liability, while others offer collaborative models where you can configure risk thresholds while the provider manages enforcement.

You should also retain full ownership of merchant relationships and transaction data, while supporting regulations such as GDPR and CCPA. This ensures you can scale your payment systems without adding compliance overhead.

Pricing models and revenue sharing structures

Your pricing model determines whether payments drive revenue or stay a cost. The priority is choosing a structure that gives you clear visibility into margin and control as you scale.

Most vertical SaaS platforms use interchange-plus pricing because it exposes the true cost of each transaction and makes margin predictable. Flat-rate pricing is simpler but hides costs. Revenue share structures vary—some give you more control than others, so the key question is always: can you see exactly what you're earning on every transaction?

Whatever model you choose, you need visibility into fees, fraud costs, and chargebacks. Without that, you can’t optimize. This is where platforms like Rainforest stand out. With transaction-level reporting, you can see exactly where margin is generated and adjust pricing over time.

What are the best practices for implementing embedded payments in vertical SaaS?

Successful implementation is what turns embedded payments from a feature into a meaningful revenue driver. For vertical SaaS platforms, the goal is to launch quickly, minimize friction, and build a scalable payment experience that supports long-term growth.

That comes down to three areas: onboarding, payment method selection, and ongoing revenue optimization.

1. Design an efficient onboarding experience

Keep onboarding focused on speed to first transaction to reduce drop-off and accelerate time-to-revenue. Collect only essential information upfront, such as business name, EIN, and bank account, and defer the rest.

Pre-built components can accelerate this. Rainforest’s Component Studio provides white-labeled onboarding flows you can customize and launch in days instead of building KYC and identity verification from scratch.

2. Choose payment methods based on your vertical

Match payment methods to how your merchants get paid:

- B2B, high-ticket: prioritize ACH and cards with invoicing

- Consumer, lower ticket: prioritize cards and wallets like PayPal and Venmo

Your integration should support all major payment rails through a single API, without separate builds for each method.

3. Optimize revenue and roll out in phases

Use pricing that gives you control over margin. Most platforms choose interchange-plus with a clear markup over bundled rates.

Roll out in phases to reduce risk:

- Start with new merchants

- Migrate your most engaged customers

- Transition the remaining base once the experience is proven

Track transaction-level profitability from day one to refine pricing and focus on your highest-margin segments.

Platforms that generate the most payment revenue treat implementation as an ongoing process, not a one-time launch. They start with core capabilities, get to market quickly, and use real-time payment data to refine pricing, improve adoption, and optimize margin over time.

With the right payments technology in place, you can move from launch to revenue faster, while continuously improving performance as transaction volume scales.

Frequently asked questions about embedded payments software

How long does it typically take to integrate embedded payments into a vertical SaaS platform?

Integration timelines range from a few days to several months, depending on your approach and provider. With modern API-first platforms and pre-built components, many software platforms can launch in days.

Rainforest provides white-labeled, drop-in payment interfaces, so you don’t need to build the UI from scratch. Custom builds or migrations typically take 4–12 weeks.

What compliance requirements must vertical SaaS companies meet when offering embedded payments?

Platforms must meet PCI DSS requirements, complete KYC and KYB for each customer, and support ongoing AML monitoring. The right embedded payments software handles most of this for you, reducing the need to build internal compliance workflows.

Rainforest maintains PCI Level 1 certification and manages ongoing compliance, helping software platforms scale their payment systems without adding operational overhead or compromising security.

Can embedded payments software handle industry-specific payment scenarios and regulations?

Yes. Embedded payments software should support vertical-specific workflows, compliance requirements, and transaction types. Whether you serve healthcare providers, fitness studios, or field service businesses, your payment capabilities need to reflect how those businesses manage online payments.

Rainforest works with vertical SaaS platforms to configure underwriting, payment methods, and reporting around real-world use cases. This includes support for subscriptions, split payments, and other industry-specific requirements.

Start earning revenue from your payments with Rainforest

Embedded payments software transforms your vertical SaaS platform from a payment facilitator into a scalable revenue generator. By owning your payments stack, you capture transaction margin, control the customer experience, and keep your data and relationships in-house.

Rainforest is an embedded payments provider that’s purpose-built for vertical software platforms that want to launch quickly and scale efficiently. A single integration connects you to cards, ACH, and wallets, while white-labeled components help you go live in days. Transaction-level profitability reporting shows you exactly what you're earning on every payment.

With built-in compliance, real-time reporting, and full visibility into your payment systems, you can start generating revenue faster and optimize as you grow.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

.avif)

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc