Embedded vs. integrated payments for SaaS: why the model you choose matters

May 11, 2026

Blog

Payments is one of the largest untapped revenue drivers in vertical SaaS platforms. But many software companies still treat payment processing as an add-on instead of a core part of their product.

Whether you capture that revenue or give it up depends entirely on your payment model.

The choice between embedded payments and integrated payments directly shapes your processing volume, margins, and merchant retention. It also affects your customer experience, checkout flow, and how easily you can streamline workflows across your platform.

Get it right, and payments become a scalable growth engine with new revenue streams. Get it wrong, and you hand off control and revenue to third-party providers.

This guide breaks down the technical and business differences between these payment solutions, so you can choose the model that improves adoption, increases volume, and maximizes payments revenue.

What’s the difference between embedded vs. integrated payments?

The core distinction between embedded vs. integrated payments comes down to where the payment experience lives.

Embedded payments are fully native, white-labeled experiences built directly into your platform. Merchants onboard, accept payments, and view reports without ever leaving your environment.

Integrated payments rely on third-party payment providers. They redirect users to external pages or separate applications to complete transactions. This breaks the workflow and weakens your platform’s value proposition.

For vertical SaaS platforms, this distinction directly impacts processing volume, margins, and retention. When merchants bounce between your platform and an external payment provider, adoption drops. They abandon onboarding, process lower volumes, and treat payments as separate from your core software rather than a unified solution.

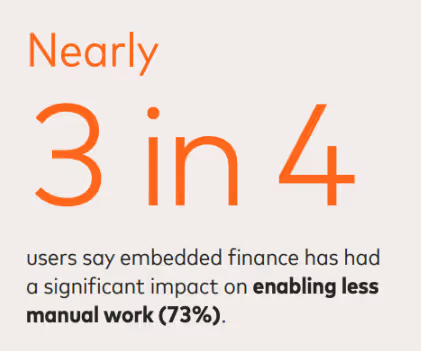

That friction isn’t theoretical. Mastercard found that embedded finance users report a 73% reduction in manual work and the same improvement in accuracy. This demonstrates how much efficiency is lost when payments sit outside your platform.

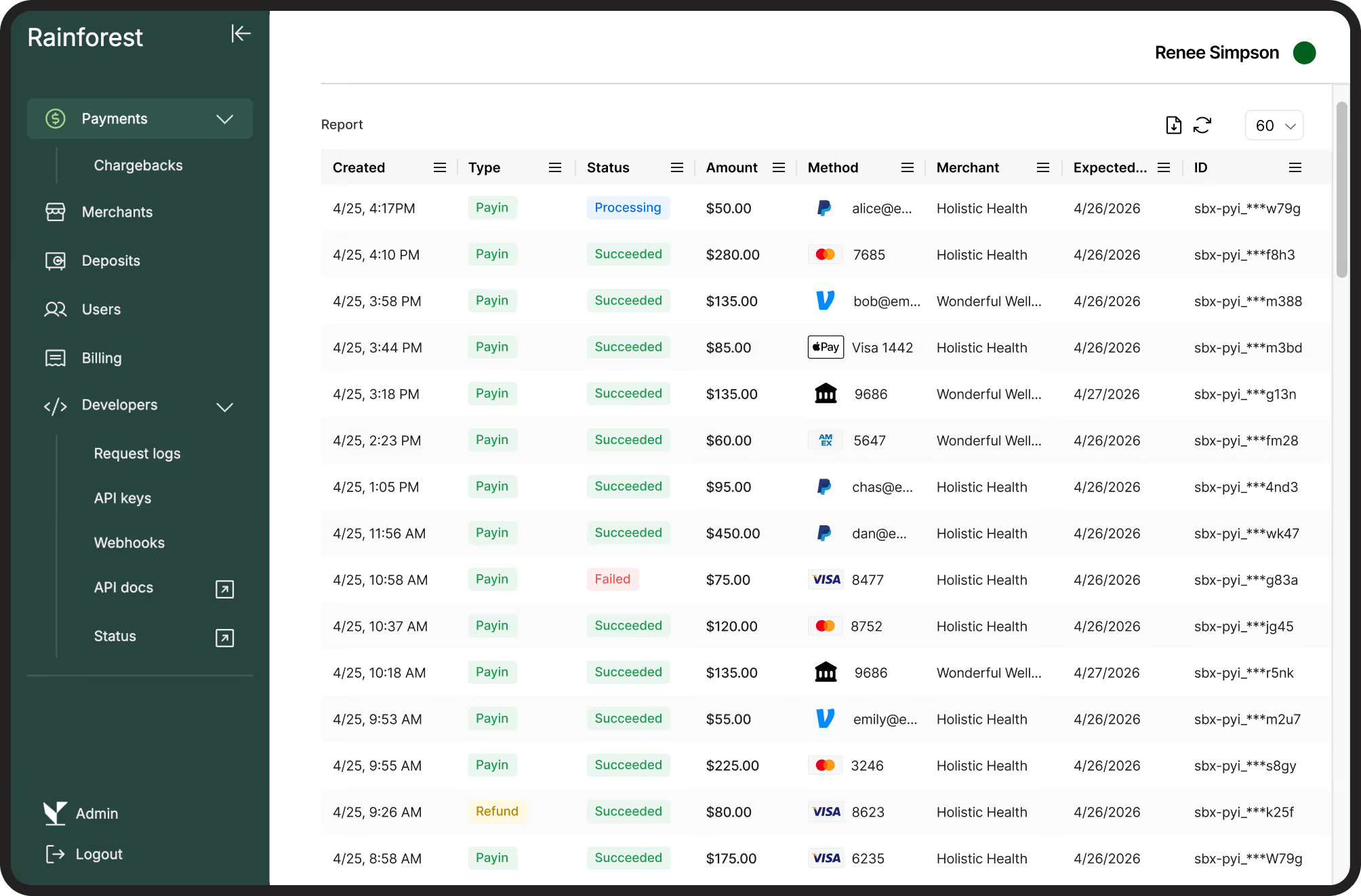

Rainforest's embedded payments solution keeps all merchant onboarding, payment processing, and reporting within your platform's brand experience. You maintain complete control of the merchant relationship, transaction data, and pricing while Rainforest handles compliance, risk, and infrastructure.

With a single API integration, you can launch in days, not months, with transparent, real-time reporting that gives you transaction-level profitability visibility from day one.

Embedded payments processing flow

Using embedded payments, the entire payment system runs inside your platform. Your merchant never leaves your interface, never sees a third-party brand, and never questions who owns the payment relationship.

Merchants complete onboarding, KYC, and underwriting through white-labeled forms that match your brand. Data flows through a single API to your payments partner, where compliance checks and account setup happen behind the scenes while you maintain full visibility.

Payment forms appear as native UI components. Card payments, ACH, and other payment methods are processed in-platform, with confirmations and reporting tied directly to your product.

When merchants need support, they contact your team, not a third-party help desk. You own the relationship completely, which improves customer experience, reduces churn, and opens the door to additional payment services and monetization.

Integrated payment processing flow

With integrated payments, merchants interact with third-party providers outside your platform.

They click a payment link, get redirected to an external page displaying the provider's branding, complete the transaction, then return to your platform—often with a delay that creates friction.

Key characteristics of this flow include:

- External redirects that break workflow continuity

- Third-party branding at the point of payment

- Limited access to payment information and reporting

- Separate merchant relationships where the provider often owns the direct account

This fragmented setup creates real operational challenges. Merchants who hit redirects during onboarding are less likely to complete setup. Those who do get through the setup process often deal with disconnected reporting and reconciliation issues.

And because the payment experience lives in the provider's system, you can't adjust onboarding fields, modify KYC workflows, or tailor the interface to match how your merchants actually operate. That makes it harder to optimize adoption, streamline workflows, and scale revenue over time.

How do embedded and integrated payments work for vertical SaaS?

According to Visa’s 2026 Embedded Finance report, software platforms are becoming the primary way businesses access financial services, shifting control away from traditional providers and into SaaS ecosystems.

That shift makes the underlying payment model critical. It determines who owns the merchant relationship, how revenue flows, and how much control your platform retains as you scale.

Technical implementation requirements

With embedded payments, you integrate once through a single API covering onboarding, payment processing, KYC, PCI compliance, and reporting. Rainforest delivers white-labeled components that plug into your platform, so your team focuses on configuration rather than building complex payment systems from scratch.

Implementation typically takes days to weeks, not months.

Integrated payments require your team to build and maintain connections to multiple third-party systems, often with separate APIs for onboarding, processing, and reporting. Each comes with its own authentication, error handling, and version management.

That means more engineering effort, higher maintenance, and longer timelines. Custom redirect flows, data syncing, and fragmented workflows can stretch implementation to 6-12 months, introducing long-term technical debt.

Integrated payments split the relationship across systems.

The payment processor owns the merchant account, controls the onboarding process, and often handles support directly. Merchants are redirected to external pages, interact with unfamiliar interfaces, and see third-party branding at critical conversion points.

Every redirect creates friction. Each additional step reduces conversion, because every external touchpoint creates a drop-off opportunity.

User experience and interface control

Embedded payments keep merchants inside your platform, creating a seamless user experience.

The payment form, checkout flow, and receipt all carry your brand. Merchants onboard through your interface, accept payments inside your software, and view transaction data in your reporting dashboard.

Revenue models and fee structures

When you embed payments, you control the economics.

You own the merchant relationship, set the pricing, and capture the full revenue spread between what you charge and your underlying processing costs. This creates scalable revenue streams tied directly to platform usage.

Most embedded platforms use interchange-plus, flat-rate pricing, or tiered pricing based on merchant size or transaction volume. With Rainforest, you get transparent transaction-level profitability reporting that shows exactly what you're earning on every payment, so you can optimize margins as you grow.

Integrated models cap that upside. They typically offer referral fees or revenue-share agreements, often in the 10–30% range of the provider’s margin. While easy to launch, this model caps long-term revenue and reduces control over pricing, payouts, and cash flow.

Over time, that trade-off becomes significant. As volume scales, platforms that use integrated payments give up more value to third-party providers instead of capturing it themselves.

Key differences between embedded and integrated payment solutions

The difference between embedded payments and integrated payments comes down to control, speed, and long-term revenue. Each model affects your time-to-market, payment experience, and ability to capture margin as your platform scales.

When to choose embedded payments

Embedded payments are the right choice when you want to maximize revenue, control the customer experience, and drive higher adoption.

Choose embedded payments if you want to:

- Capture the full margin on every transaction

- Maintain control of merchant relationships and transaction data

- Increase adoption and total processing volume

- Improve retention and lifetime value through platform stickiness

- Support future embedded finance products like lending or expense management

Best fit for:

- Platforms with meaningful payment volume

- Verticals with specific workflows (e.g. card-on-file, invoicing)

- Teams treating payments as a core revenue driver

Modern platforms like Rainforest remove the traditional barriers. With one API, you can launch fully embedded, white-labeled payment solutions in days while outsourcing compliance, risk, and infrastructure.

When to choose integrated payments

Integrated payments make sense when speed and simplicity matter more than control or revenue.

Choose integrated payments if you want to:

- Launch quickly with minimal development work

- Test payment monetization before investing further

- Avoid adding payments complexity to your roadmap

Best fit for:

- Early-stage SaaS platforms validating demand

- Teams with limited engineering bandwidth

- Use cases where payments are not core to the product

Trade-off:

You give up control of the payment experience and a significant share of the revenue. As volume grows, this model limits scalability and reduces your ability to optimize pricing and margins.

Which payment approach is right for your vertical SaaS platform?

Your payment approach comes down to four main factors:

- Platform maturity

- Technical resources

- Revenue goals

- How central payments are to your customer experience

Integrated payments may be enough if:

- You process less than $5M annually

- Payments are not core to your product

- You need to launch quickly with minimal effort

Embedded payments are the better choice if:

- Payments drive merchant retention

- You want to own the merchant relationship and transaction data

- You are focused on maximizing long-term revenue and scalability

- Your users expect unified workflows and a seamless checkout experience

Rainforest removes the traditional tradeoff. You get full white-label control and revenue optimization without a 12–18 month build.

The revenue impact

Revenue goals should drive your decision.

- Integrated payments: typically 10–20 basis points via referral fees

- Embedded payments: often 50–100+ basis points depending on your model

For a platform processing $50M annually, that difference can mean:

- $200K–$500K in additional revenue

As volumes grow, the gap widens. Most mid-market and enterprise SaaS platforms see stronger unit economics, improved cash flow, and higher lifetime value with embedded payments.

Implementation considerations and best practices for vertical SaaS

Choosing the right payment approach is only half the battle. Successful implementation requires planning that keeps revenue optimization and operational efficiency front and center.

Before you launch:

- Map your onboarding flow (KYC, underwriting, account setup)

- Define your pricing and revenue model early

- Confirm your provider handles PCI, fraud, and chargebacks

As you roll out:

- Build reporting into your product from day one

- Prepare your support team for payments-related questions

- Align engineering, product, and finance on adoption and volume goals

Modern embedded payment solutions, like Rainforest, simplify this process. Rainforest handles compliance, risk, and infrastructure while you maintain full control of merchant relationships and data.

The most successful platforms treat payments as a revenue strategy, not just a feature.

Start earning payments revenue with a purpose-built approach

Your choice between embedded and integrated payments is a revenue decision. It shapes your processing volume, margins, and long-term platform differentiation.

Embedded payments give you full control of the merchant relationship, transaction data, and payment experience. That control drives higher adoption, stronger retention, and more predictable new revenue streams.

Integrated payments do the opposite. They push merchants to third-party experiences, limit visibility, and cap your revenue through shared economics.

Rainforest is purpose-built for vertical SaaS platforms that want to maximize payments revenue without building infrastructure from scratch. With fully embedded, white-labeled components, real-time transaction-level profitability reporting, and collaborative underwriting, you can scale volume and margins while maintaining control. The platforms that win treat payments as a core product and monetization strategy.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc