SaaS fraud prevention that scales with your platform

June 12, 2026

Blog

SaaS platforms with embedded payments face fraud risks that most software companies never encounter. You're onboarding real merchants, processing real transactions, and managing embedded payments workflows that fraudsters actively target. When fraudulent accounts slip through onboarding, process payment fraud, and disappear before chargebacks arrive, the financial losses hit your platform directly.

Many payment providers push fraud liability back onto SaaS platforms through unclear contract terms and limited fraud protection. That leaves teams managing chargebacks, suspicious activity, customer trust issues, and operational costs at the same time.

Strong SaaS fraud prevention combines identity verification, fraud detection, behavioral analysis, and real-time monitoring to protect revenue as your platform scales.

What does fraud look like in vertical SaaS?

Vertical SaaS platforms are attractive fraud targets because they onboard merchants, process payments, and operate within predictable industry workflows.

Many horizontal acquirers built for direct merchants, including Stripe, Adyen, and Braintree, adapted their fraud prevention models to support platforms later. Rainforest built its fraud infrastructure specifically for vertical SaaS, allowing rules and risk scoring to reflect real industry behavior instead of generic ecommerce patterns.

Platforms running embedded payments often don't realize they're exposed to fraud losses until chargebacks start climbing. Rainforest's fraud monitoring rules are tuned for the platform's specific vertical and merchant behavior, not cranked tight to protect the provider from a loss it isn't carrying.

Common fraud patterns across the account lifecycle

Fraud in vertical SaaS usually develops across onboarding, transaction activity, and chargebacks rather than in a single event.

Common patterns include:

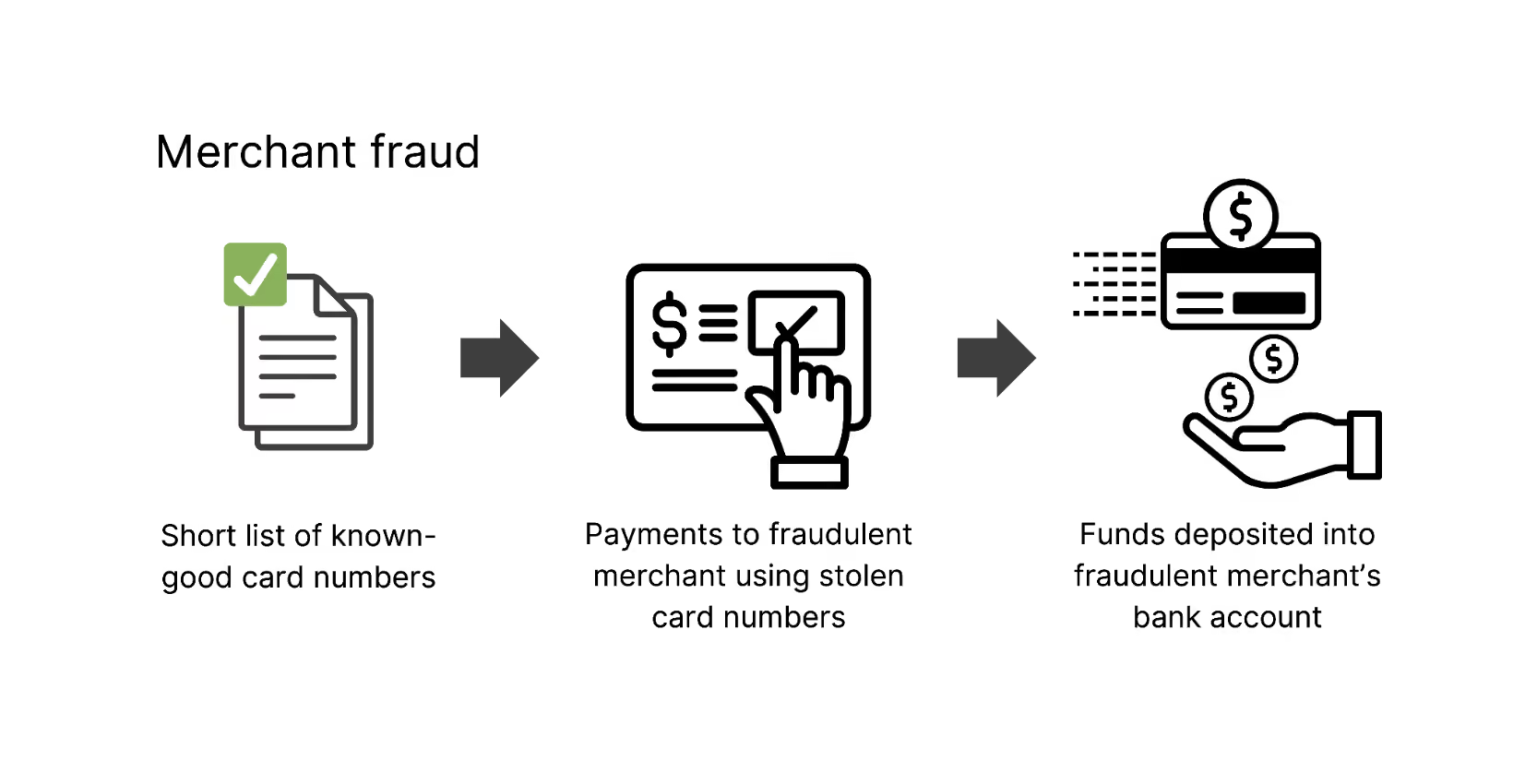

- Account creation fraud: Fraudsters use stolen or synthetic identities, fake business documents, or repeated device and IP data to create merchant accounts. This is extremely common. According to Veridas’ 2024 Identity Fraud Report, 85% of financial fraud cases now involve synthetic identities.

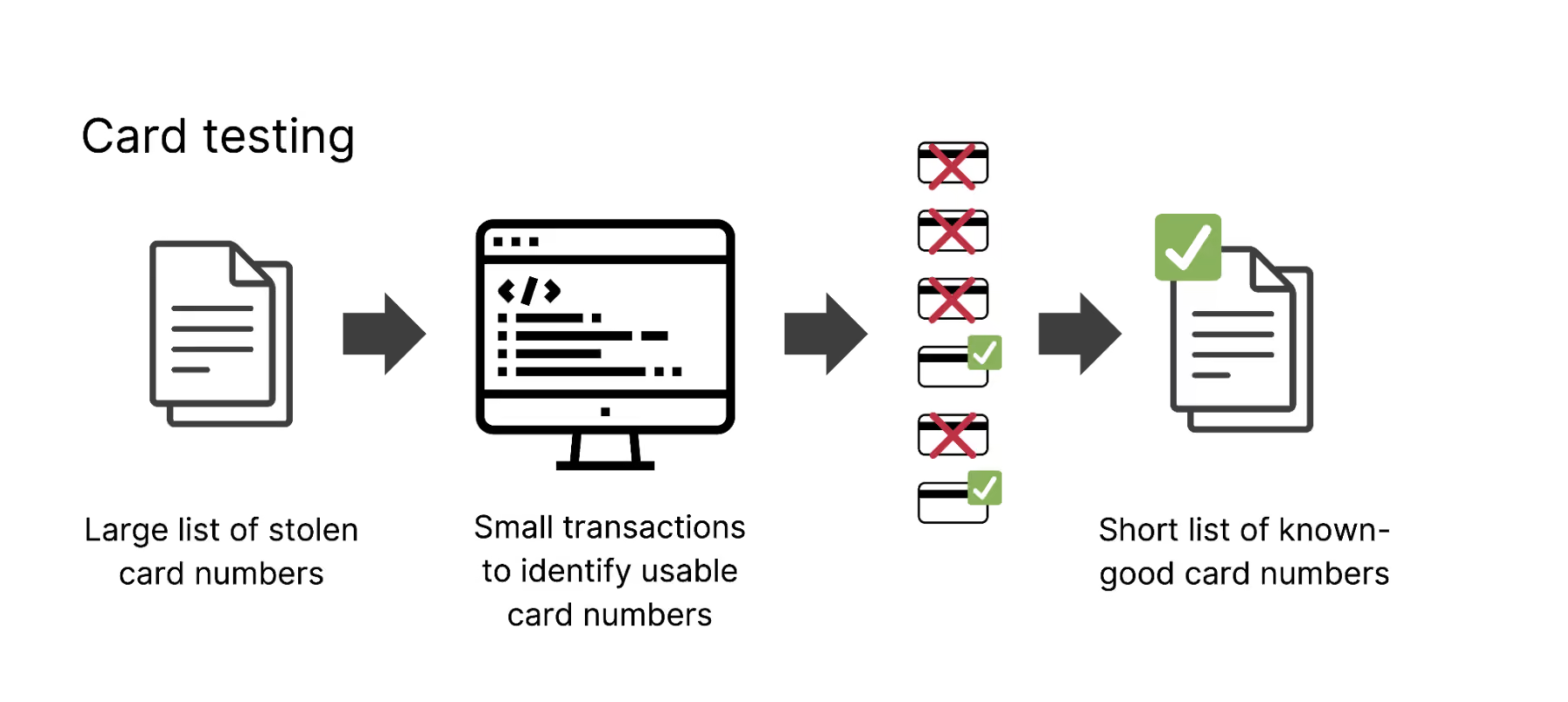

- Transaction testing: Small transactions test whether stolen payment methods work and whether fraud controls trigger alerts.

- Velocity abuse: New merchants suddenly process unusually high payment volume shortly after onboarding.

- Chargeback schemes: Fraudulent merchants process stolen card payments, disappear, and leave platforms dealing with disputes weeks or months later. Industry fraud reports show how difficult these disputes are to recover once they reach the chargeback stage. Verifi’s 2024 Global Fraud and Payments Report found that merchants reported win rates below 20% on fraud-coded chargeback disputes.

The biggest risk is delayed visibility. Many platforms fail to connect onboarding signals, transaction behavior, and chargeback activity until fraud losses have already scaled.

Early warning indicators your platform is being targeted

Fraud usually appears in behavioral patterns before it appears in reconciliation reports or chargeback data.

Look out for:

- Sudden spikes in merchant signups

- Repeated signups from the same device or IP address

- Sequential email addresses or cloned business details

- Multiple declined transactions followed by successful charges

- Geographic mismatches between merchants and transaction activity

- Chargeback ratios climbing above normal thresholds

Identifying key signals for effective SaaS fraud prevention

Effective SaaS fraud prevention depends on monitoring signals across onboarding, merchant activity, and payment behavior. The most important signals fall into three categories: identity and signup, behavioral and usage, and billing and network.

Identity and signup signals

Identity signals appear during onboarding before a merchant processes transactions.

Watch for:

- Free email accounts tied to high-value businesses

- Phone numbers that don't match business locations

- Repeated signups from the same IP address or device

- Business names or addresses that fail verification checks

These signals help identify fake accounts, synthetic identities, and onboarding abuse early. Providers that handle KYC, merchant verification, and onboarding checks automatically reduce operational overhead and compliance risk.

Behavioral and usage signals

Merchant behavior often reveals fraud after onboarding.

Common warning signs include:

- Sudden spikes in payment volume

- Multiple failed login attempts or unusual login locations

- High refund or chargeback rates

- Merchants using payments features while ignoring the rest of the platform

Behavioral analysis is especially important in vertical SaaS because transaction patterns vary widely between industries. A field services platform behaves differently from a fitness or healthcare platform, and fraud rules should reflect that.

Billing and network signals

Billing and network signals track how money moves through your payments ecosystem. Watch for:

- High card decline rates

- Rapid changes in payment methods

- Rising chargeback ratios

- Unauthorized transaction disputes

- Card testing behavior

Most card networks enforce chargeback thresholds around 1%. Platforms that monitor billing activity and suspicious payment behavior in real time catch fraud earlier and reduce downstream fraud losses.

Rainforest monitors these signals as part of its embedded payments stack so you're not left interpreting network alerts or holding chargebacks on your own.

Implementing fraud controls without harming conversion

The hardest part of running embedded payments is stopping fraud without killing conversion. Every fraud prevention control you add creates friction. Too much, and legitimate merchants abandon onboarding. Too little, and you absorb chargebacks, fraud losses, and operational costs that compound fast.

Generic fraud rules from legacy providers throttle conversion because they're built for horizontal use cases, not your vertical. A contractor platform where merchants process large invoices weekly looks nothing like a retail marketplace with thousands of small daily transactions, and your risk scoring, authentication, and fraud rules need to reflect that reality.

Rainforest tunes fraud rules collaboratively with the platform, using real merchant data and transaction patterns from the platform's vertical rather than generic ecommerce baselines. Because Rainforest only earns when the platform's merchants succeed, the incentives align: both parties want maximum legitimate volume and minimum fraud risk.

That tuning happens with a named team that knows your vertical, not a ticket queue. Rule changes get made in a working session, not a support thread, and the same person who configured your onboarding flow sees the chargeback report a month later.

See how Rainforest secures your payments

The friction ladder: matching response severity to risk level

Not every fraud signal deserves the same response. A mismatched billing address might warrant a simple verification step, while a spike in chargebacks from a single merchant should trigger an immediate hold. The friction ladder matches the severity of your response to the level of risk detected.

- Low friction (automated): Email or phone verification at signup, address verification service (AVS) checks, device fingerprinting, velocity checks on account creation

- Medium friction (manual review or user action): Document upload for identity verification, temporary transaction holds, step-up authentication for high-value actions, manual underwriting for accounts flagged by multiple signals

- High friction (immediate intervention): Account suspension, transaction blocking, or permanent removal for confirmed fraudulent activity

The goal is to stop suspicious activity without damaging the user experience for legitimate merchants. Rainforest tunes this ladder to your vertical during onboarding, so thresholds reflect real risk patterns in your industry rather than generic baselines that cost you revenue.

Building and scaling your SaaS fraud prevention program

Building a vertical SaaS fraud prevention program doesn't require a large fraud ops team from day one. The goal is to put enough controls in place to reduce fraud risk, protect revenue, and support growth without creating unnecessary operational overhead.

Your first 60 days: a minimum viable program

A basic fraud program should focus on three areas:

- Identity verification during onboarding

- Transaction and payment fraud monitoring

- Chargeback tracking across merchant accounts

Start with KYB and KYC checks during onboarding. KYB validates the business entity (legal name, EIN, address) against public records and watchlists. KYC validates the individuals behind it (signatories and beneficial owners) against ID, address, and sanctions screening. Flag suspicious activity for manual review instead of auto-rejecting legitimate merchants too aggressively.

Next, add transaction velocity and behavioral monitoring. Watch for:

- Large payment spikes from newly onboarded merchants

- Repeated failed payment attempts

- Multiple accounts tied to the same device or IP address

- Sudden increases in refunds or chargebacks

Even a simple dashboard tracking disputes, refund rates, and transaction anomalies can help identify fraud patterns before they become expensive fraud losses.

When to build vs. buy fraud prevention

The build-versus-buy decision depends on your engineering resources, scalability needs, and tolerance for operational complexity.

Building internally gives you full control over rule logic, risk scoring, workflows, and merchant experience. But it also means managing:

- False positives

- Ongoing maintenance

- Compliance requirements

- AML, PCI, and KYC processes

- Liability when fraud slips through

Partnering with a provider reduces that overhead and helps teams launch faster. Rainforest handles fraud monitoring, KYC/KYB, PCI Level 1 compliance, and embedded payments infrastructure as part of its PayFac-as-a-Service model.

Many SaaS platforms start with a partner model, then evaluate building more internal controls once payment volume and operational maturity increase.

Frequently asked questions about SaaS fraud prevention

What is SaaS fraud prevention and why does it matter for vertical SaaS?

SaaS fraud prevention combines monitoring, authentication, identity verification, and transaction controls to stop fraudulent activity across the merchant lifecycle. For vertical SaaS platforms running embedded payments, fraud directly affects revenue, chargebacks, customer trust, and compliance exposure, though much of the prevention work is shared with your payments provider. A single wave of fake accounts or stolen payment activity can increase fraud losses quickly and put your payments program at risk.

How do I reduce fraud without adding friction that hurts conversion?

Reduce friction by matching fraud controls to merchant risk levels. This works best as a collaboration with your payments provider: you know your merchants, and the provider tunes detection and risk scoring to your vertical. Low-risk merchants can move through automated onboarding, while high-risk accounts trigger additional KYC, KYB, or manual review steps. Strong fraud detection, behavioral analysis, and risk scoring help SaaS platforms stop suspicious activity without slowing legitimate merchants or damaging the user experience.

What are the first fraud controls a SaaS team should implement?

Start with onboarding verification, transaction monitoring, and velocity limits. Basic controls like identity verification, device and IP monitoring, transaction thresholds, and chargeback tracking help detect common fraud patterns early. As payment volume grows, SaaS companies and their payments provider share this work, with the provider typically handling fraud infrastructure while the platform provides data to support fraud monitoring and works with merchants to implement best practices.

Start building a fraud program that protects your platform

The cost of weak fraud controls adds up quickly. Fraudulent merchants create chargeback liability, stolen card transactions erode margins, and poor KYC processes expose platforms to compliance and operational risk.

Start by reviewing how your current payments infrastructure handles fraud detection, onboarding, transaction monitoring, and chargeback management. Identify where you already have visibility and where fraud signals are slipping through.

Rainforest's PayFac-as-a-Service model handles fraud monitoring, KYC/KYB, and PCI compliance as part of its embedded payments infrastructure, helping SaaS platforms reduce operational overhead while scaling payment volume more confidently.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

.avif)

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc