Best PayFac platforms compared for vSaaS (2026)

July 16, 2026

Blog

.png)

Embedded payments can be a major revenue line for vertical SaaS platforms. But only if the underlying PayFac or PayFac-as-a-Service model actually fits your business. Pick the wrong one and you're looking at months of engineering work, compliance overhead you didn't plan for, limited control over the merchant experience, and margins that disappear into hidden fees.

And even though most PayFac platforms market themselves to vertical software platforms, their underlying infrastructure is still built for generic payment processing. That means slow onboarding, rigid pricing, and long-term margin pressure for software platforms trying to monetize payments and grow the business.

We compared the top PayFac platforms for 2026 (including payment providers that offer PayFac-like capabilities) on what really matters. How fast you can go live, the payments infrastructure behind them, how much operational hassle you're signing up for, and who actually owns the merchant relationship when it's all said and done.

PayFac vs. PayFac-as-a-Service, explained

Embedded payments have become a real growth channel for SaaS platforms. In fact, the embedded finance market is projected to pass $228 billion globally by 2028 as more software companies monetize payments inside their products.

Here's how the models break down.

A PayFac (payment facilitator) is a registered entity that onboards sub-merchants under its own master merchant account. They are the primary owner of the entire payments infrastructure, including compliance, risk management, underwriting, chargebacks, and fraud monitoring.

PayFac-as-a-Service (PFaaS) gives vertical SaaS companies a faster path in. Instead of building the payments infrastructure yourself, you integrate through an API while your payments partner handles compliance, risk management, and underwriting behind the scenes.

You still own the merchant relationship. You still capture payments revenue. The difference is operational overhead. Full PayFac registration takes more than a year and needs dedicated payments operations and compliance staff. With a PFaaS provider, SaaS companies can go live in weeks.

That speed matters. Embedded finance market growth in the US is expected to reach $140 billion by 2030, driven largely by software platforms building payment solutions directly into their products.

The best PayFac platforms? They’re the ones built to boost revenue for vertical SaaS companies.

Seamless merchant onboarding, flexible pricing, embedded payments, and revenue models that scale with transaction volume.

How we evaluated the best PayFac platforms for vertical SaaS

This comparison isn't a generic feature checklist. It's built around the criteria that actually matter when you're running payments at scale.

- Go-live speed. Time-to-market decides how fast you start capturing revenue.

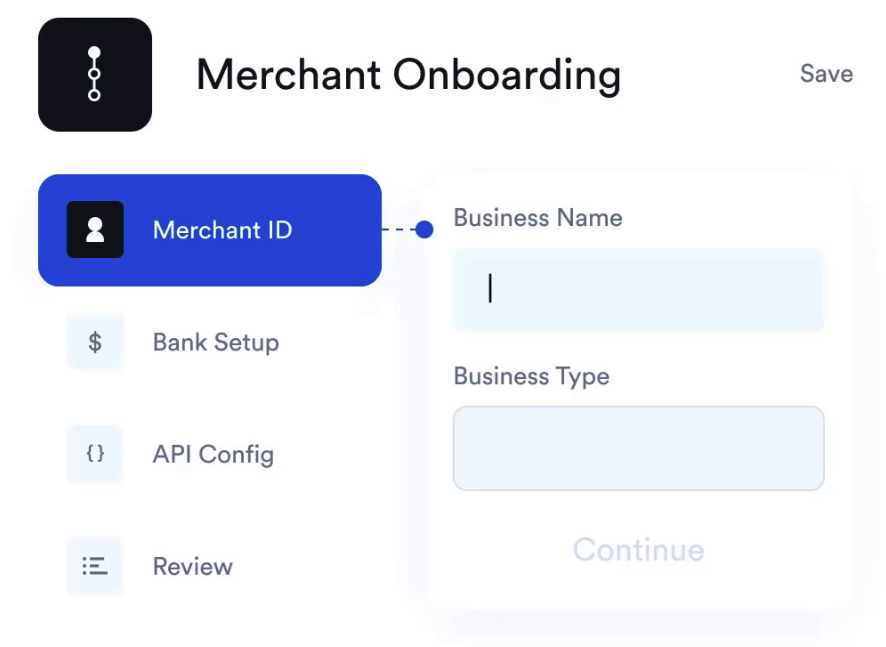

- Merchant onboarding. Onboarding UI quality, and whether the platform ships white-labeled components or forces you into custom builds.

- Payment methods. Most platforms handle basic card payments. We looked at ACH, digital wallets (Apple Pay, Google Pay, PayPal, Venmo), and whether adding methods means signing separate contracts.

- Commercial model. How each platform structures pricing. Interchange-plus vs. flat-rate models, and whether you get to set your own merchant pricing or not.

- Compliance and risk handling. Who holds the compliance burden, who absorbs which losses, and how much operational overhead lands on your team.

- Contract flexibility. Contract length, termination clauses, and whether you keep ownership of your merchant data if you switch providers.

- Pricing transparency. Hidden fees make unit economics impossible to model. We prioritised platforms with clear pricing or detailed cost breakdowns.

- Vertical SaaS fit. Whether each provider understands your business model and builds their product around helping you grow payments revenue, or treats you like every other customer.

The best PayFac platforms for vertical SaaS in 2026

These six PayFac platforms take meaningfully different approaches to embedded payments and payment processing. Which one fits comes down to your engineering capacity, your compliance appetite, and your revenue goals.

Watch out for legacy providers in this space. They'll run on outdated infrastructure, and barely offer any vertical-specific support. All three of these hold back your ability to grow payments revenue.

Rainforest: Best for fast go-live, purpose-built for vertical SaaS

Rainforest is purpose-built for vertical SaaS platforms that want to start processing payments in days, not months. One API and white-label, low-code components handle merchant onboarding, payment acceptance, reporting, dashboards, and chargebacks. No separate integrations required.

What you get:

- One integration for every payment method. Cards (debit and credit), ACH, Apple Pay, PayPal, Venmo, PayPal Pay Later, and card-present terminals, all through a single API.

- End-to-end compliance. KYC, PCI, fraud monitoring, and risk management, so your team stays focused on product and growth.

- Full ownership of your merchant data, relationships, and sell price. No exclusivity or non-solicits. No tokens taken hostage. No surprises at contract renewal.

- Merchant credit losses absorbed. Rainforest is responsible for merchant underwriting, which means we absorb the losses. Fraud-driven chargebacks can be reduced through built-in tools like 3DS.

- A support team that knows your business. Real humans, with experience and expertise, are empowered to resolve your issues. Not a ticket queue or AI chat.

- Go-live in days, not months. From contract signature to first transaction.

- Transparent IC+ pricing with penny-perfect reporting. You set your merchant pricing and keep the spread. No hidden fees.

We only make money when your merchants do. So this feels less like hiring a vendor and more like having your own payments team looking out for you.

Stripe Connect: Best for developer-first platforms that want a self-serve model

Stripe Connect gives engineering teams flexible building blocks for embedded payments.

What you get:

- Extensive documentation, embeddable components, modular APIs, and developer-friendly SDKs

- Broad payment method support across 135+ currencies and global payment flows

- Custom onboarding flows, merchant dashboards, and integration with Stripe's broader payments ecosystem and financial product suite

The tradeoffs:

- Originally built for e-commerce merchants and later retrofitted for platforms

- Largely designed for a self-service rather than full-service model

- Outside of the largest platforms (typically billions in TPV), Stripe typically doesn’t provide extra guidance on interchange optimization, program management, pricing strategy, etc.

- Lack of clarity on who owns risk can lead to gnarly surprises

- Limited flexibility around merchant billing for payments

- Support is provided using mass-scale methodologies vs boutique and personalized

- Direct merchant sales channel can lead to channel conflict

Best suited for platforms that want a self-service model.

Finix: Best for platforms that need a high-risk processor

Finix provides infrastructure for platforms that want to register as a full PayFac and own the entire payments stack, though they now also offer a PayFac-as-a-Service option.

What you get:

- Sponsor bank relationships

- High-risk processing

- Pricing flexibility

The tradeoffs:

- Originally built as an infrastructure product for registered PayFacs and later pivoted to managed PayFac offering

- They sell directly to merchants which can lead to channel conflict

- Ambiguity around risk ownership can lead to unexpected risk losses

Best for platforms with a large proportion of high-risk merchants. If considering the registered PayFac option, review the hidden costs of becoming a PayFac. The control is real, but so is the overhead.

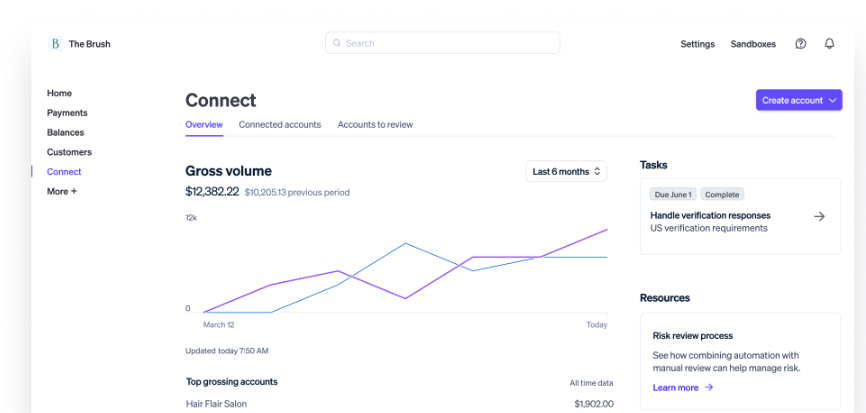

Adyen for Platforms: Best for very large platforms with truly global merchant bases

Adyen for Platforms suits SaaS companies processing payments across multiple countries.

What you get:

- Support for 250+ payment methods globally

- Local acquiring in 30+ markets

- Unified reporting across geographies

- Sub-merchant onboarding with built-in KYC and jurisdiction-specific risk monitoring

The tradeoffs:

- Robust technical stack requires significant customization, integration complexity, and ongoing maintenance

- Business focus is mainly on large multinational merchants which means Adyen for Platforms can be left competing for resources

- Limited risk tooling for platforms and managed risk offering often comes at a higher cost and lower approval rates

- Tech stack requires a significant amount of maintenance and work

Best suited for platforms already processing significant volume (e.g. billions or tens of billions), where global merchants comprise a significant share of that volume.

Tilled: Best for platforms that want to outsource support

What you get:

- Merchant onboarding, KYC, PCI compliance, and chargeback management handled for you

- White-labeled merchant support (on the Enterprise plan)

- A revenue share model with no compliance or underwriting responsibilities

The tradeoffs:

- Monthly SaaS fee and revenue share limit platform upside

- White-label merchant support sounds like a value-add, but offloading support to a payment provider can undermine merchants’ trust in platform and can actually create more support challenges if not executed well

- By not becoming a registered PayFac, there are extra middlemen involved in all transactions and Tilled has effectively given up control of risk and underwriting to upstream partners

Works best for platforms that want to offload support to a payment provider.

What the feature matrix doesn't tell you

The factors that decide whether embedded payments actually work for your business sit outside the feature matrix. It’s actually in the fine print, risk allocation, and the operational realities you only find out about after you've gone live.

Contract terms and exit flexibility. Before you sign, ask what happens if you outgrow the payment provider. Can you move your merchant portfolio, or are you stuck? Rainforest is built around platform-friendly terms. Full ownership of merchant data, relationships, sell price, and experience. And you own your data.

Legacy processors can trap you with token export fees and non-solicit clauses that extend beyond the contract term. Check how easy it is to leave before you sign, not after.

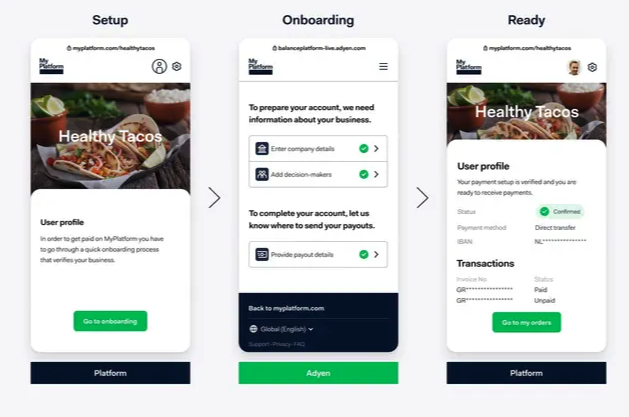

Who owns the merchant relationship. Some providers wedge themselves between you and your merchants, controlling onboarding flows and communication. Rainforest white-labels the entire payments experience. Merchants onboard under your brand, see your logo, and talk to your support team.

Who absorbs which losses. Most payments partners monitor fraud and report chargebacks, but the loss allocation varies more than the marketing implies. Chargebacks sit with the merchant. That's how the card networks work. Some fraud-driven chargebacks are preventable, and the tooling your payments partner offers to reduce them (like 3DS) shapes how many your merchants see. Merchant credit losses are different. When a merchant goes under and their customers dispute the payments, someone has to absorb that loss. Since Rainforest is responsible for merchant underwriting, we also absorb merchant credit losses. This matters when you're scaling volume and can't predict which merchants will make it.

Transaction-level profitability reporting. The best PayFac platforms give you visibility into margin per transaction, per merchant, and per payment method. Rainforest makes this data available in your residual report, so pricing decisions sit on actual data instead of estimates and averages. This is the difference between running payments as a real product line and running it as a black box.

Do you really need global processing? A processor with support for dozens of international markets might make sense for a platform with billions in processing volume in several markets. However, a platform with concentrated volume in 1-3 markets and a smaller share of volume in other markets would usually be better served by choosing the best payment provider in each of their 1-3 largest markets, plus a low-lift global processor for the “long tail” markets.

Frequently asked questions about PayFac platforms

What is the difference between a PayFac and a PayFac-as-a-Service provider?

A PayFac is a registered entity that takes on full liability for sub-merchant underwriting, compliance, and risk management. A PFaaS provider runs all of that underlying infrastructure for you, so you can offer embedded payments without becoming a registered PayFac. Most vertical SaaS platforms go the PFaaS route because it gets you live faster, costs less upfront, and keeps your team focused on the product.

How long does it take to go live with a PayFac platform as a vertical SaaS company?

Go-live timelines range from days to more than a year, depending on the model you pick. Purpose-built PFaaS providers like Rainforest can get you processing in as little as days through a single API and pre-built embeddable components for merchant onboarding, payment acceptance, reporting, and more. Developer-first platforms like Stripe Connect take months with dedicated engineering resources. Full PayFac registration usually runs at least 12 to 18 months end-to-end, requiring sponsor bank approval, infrastructure buildout, registration with the card networks, and compliance.

How do PayFac platforms make money, and how does that affect my margins?

PayFac platforms earn through per-transaction fees, basis point buy-rates on payment volume, monthly platform fees, and revenue shares. Most charge actual passthrough costs plus a wholesale buy-rate and let you set your sell price to merchants. The spread is your margin. Some providers layer on hidden fees like PCI compliance charges that eat your effective revenue share and make profitability harder to forecast. Rainforest uses transparent IC+ pricing with transaction-level passthrough cost detail and merchant-level profitability reporting. So you see the actual margin as you scale.

Choose the right PayFac platform and start earning payments revenue

Pick the platform that actually fits your timeline, engineering team's bandwidth, your risk appetite, and your revenue model. Most players in this space are still stuck with rigid contracts, weak vertical support, and outdated tech. And that just doesn't cut it when payments are a real revenue driver.

Purpose-built software deserves purpose-built payments. Rainforest helps vertical SaaS platforms process more volume at higher margins, without taking on risk or compliance overhead. You keep full control of merchant data, relationships, and pricing. We handle KYC, PCI, and fraud monitoring.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc