Monetize payments for SaaS platforms: A revenue guide

July 9, 2026

Blog

Your customers are processing payments through your platform right now. And someone else is keeping the revenue.

You don't need a fintech team or a compliance department to change that. Any vertical SaaS platform that helps merchants accept payments from end-customers can turn those payments into a real revenue line. What separates the platforms that do from the ones that don't comes down to three calls:

- Pick the right monetization model and commercial terms

- Choose a provider that gives you full control over economics, merchant relationships, data, and the payment experience

- Build a payments product that helps your business customers save time, reduce administrative work, and grow their business

What it means to monetize payments for SaaS platforms

Payment monetization means you earn a share of every dollar your merchants process. You can do that through a revenue share, markup or bundled pricing, instead of handing that revenue to a third party.

Here's what that means for your platform:

- Merchants onboard inside your product

- Your software product controls the flow of funds

- Every card swipe, ACH transfer, or online checkout earns you revenue

- You own the merchant relationship, the data, the pricing, and the experience

The upside is a new revenue stream that scales with your merchants. Andreessen Horowitz found that vertical SaaS platforms embedding financial services can grow revenue per customer by 2–5x, without adding new users or products. And the money on the table adds up fast. A platform processing $50M–$500M in GMV a year, running at a modest 30-basis-point take rate, is leaving $150,000 to $1.5M in annual revenue on the table by not participating.

Revenue isn't the only payoff. Embedded finance cuts operational friction too. Mastercard research found it cuts manual work by 73%.

How to choose the right payment monetization model for your vertical

Your monetization model shapes what comes next. It determines your pricing, how merchants adopt, and how much margin you keep. Most vertical SaaS platforms pick from three structures:

1. Revenue share and referral models

Revenue share is the lightest lift. You refer merchants to a payments partner and take a percentage of the revenue they generate. It’s usually about 10–30% of net margin.

What you get:

- No compliance overhead

- Fast entry into payments revenue

- A simple economic model

What you don't get:

- The merchant relationship and data

- Control over pricing

- Any input into underwriting

This might be appealing to platforms just getting into payments, teams with limited engineering resources, or organizations that don’t want to handle tier 1 support. The math is small but real. If your partner earns 50 basis points on a merchant processing $1M annually and you earn a 30% revenue share, your share lands around 15 basis points. $1,500 a year.

But the downside is massive. And structural. The provider owns the merchant data and the relationship. They control pricing. It’s exceptionally difficult to build a high-value payments experience on a referral-based provider. And switching providers or bringing payments in-house gets harder every year you stay. Some modern payments providers guarantee the platform owns its merchant data and relationships. Legacy processors often go the other way. In extreme cases, exit costs can add up to millions, driven by data lock-in and non-solicits that extend beyond the contract term.

2. Markup and take-rate models

You set the sell price. You keep the spread between what your merchants pay and what your payments partner charges you.

Here’s a hypothetical example:

- You pay interchange, network fees, and a buy rate to your payment provider – for this example, let’s say the total effective cost is 2.4%

- You charge merchants 3.2% + $0.50

- You keep the 80 basis-point spread

This is the optimal model for most vertical SaaS platforms. Full control over pricing, merchant relationships, and revenue per transaction. From our experience, we’ve seen platforms in high-ticket verticals like field services nearly double their margins and reduce tickets by 90% with this playbook.

Rainforest gives you transaction-level reporting and margin visibility. Teams optimize pricing, merchant cohorts, and payment flows in real time. No waiting on monthly reconciliation files.

3. Bundled payments as a product feature

Bundling payments into your SaaS pricing could possibly take the adoption decision off the merchant's plate. Merchants pay a higher rate (e.g. 5%) for payment processing and the payment processing margin covers the software fee.

This works well for platforms with:

- High transaction frequency

- Deep payments integration (i.e. merchants wouldn’t even consider using the core software without payments)

- Merchants who value simplicity over rate shopping

Many platforms start with a referral-based revenue share, then move to markup or bundled pricing as transaction volume grows. However, there’s no reason that a new platform can’t start with markup or bundled pricing.

How to build a pricing architecture that drives adoption

Your pricing model can help or hinder embedded payments adoption. But important to note that the pricing itself might not be critical. In many cases, what matters more is the value of the underlying product and how you present the pricing. Similarly, the way you talk about payments in the sales and onboarding process can significantly decrease merchant price sensitivity.

Keep pricing as simple as possible to create a better merchant experience. Because complex pricing just results in complex reporting and more support requests. And complicated pricing can feel more expensive, regardless of the math.

List payments pricing alongside core software pricing. If a payments product is separate from the SaaS product, the value of payments becomes disconnected from the value of the core software product.

Limit statement analysis and pricing reviews to large merchants who are serious about the solution. Use a tiered approach to avoid a comparison for smaller merchants.

With Rainforest, you set the sell price, the contract terms, and who owns the merchant data. You control the economics, not your payments partner.

Setting your take rate: Guardrails and benchmarks

A target take rate for most vertical SaaS platforms depends on where you are in your payments journey, what you’re optimizing for, how much work you’re willing to put in. Here are some best practices to maximize revenue:

- Pick a price and run with it. And promote it to potential early adopters. Start high and make adjustments if needed.

- Focus on adoption over margin. Volume beats take rate all day, because volume is only limited by the total available market. Once you’ve found a reasonable price point, shift your focus to driving adoption.

- Optimize interchange. The best way to increase take rate is interchange optimization because the majority of card processing cost is interchange passthrough.

Both take rate and adoption start with creating value in the product. When you optimize the product, experience, and GTM motion for your customers, you might be surprised to find that you don’t have to trade off between take rate and adoption. You can have both.

Tiering by GMV band and customer segment

Different merchants process different volumes. Your pricing should reflect that.

A common structure:

- Low-volume merchants absorb the highest rates. Onboarding and operations overhead eat proportionally more at this size.

- Mid-volume merchants make up the bulk of your GMV. These merchants are often value-driven, and might be willing to pay a bit more if the payment product saves them hours every week.

- High-volume merchants can get favorable pricing by going directly to a payment processor, and are more likely to expect discounted rates (ask to review a processing statement as they may be paying significantly more than they believe)

The definition of a low-, medium-, or high-volume merchant will be specific to your platform. Keep pricing simple enough that your sales team can explain it in one sentence. Complex structures slow onboarding and create friction during contract reviews.

Handling the "we already have a processor" objection

This is the most common objection when rolling out embedded payments. And competing on rate alone almost always fails.

Focus on operational friction instead. When payments live outside your platform, merchants deal with:

- Separate logins

- Manual reconciliation

- Disconnected reporting

- Slower support workflows

Position embedded payments as the fix. One workflow, inside the software your merchants already live in.

The best conversion window opens 60–90 days before an existing processing agreement renews. Merchants are already reviewing terms at that point, which means they're far more open to switching if the workflow and economics improve.

What you own versus what your payments partner owns

The split between your platform and your payments partner shapes three things: your compliance exposure, your operational overhead, and your long-term margin.

You own:

- Merchant relationships and contract terms

- The product and payment experience

- Adoption strategy, pricing, and revenue

Rainforest handles:

- Merchant onboarding, KYC/KYB, and underwriting

- Payment security compliance and data protection

- Fraud monitoring and risk management

- Chargebacks, disputes, and payouts

Most platforms assume their payments provider absorbs fraud losses. Most don't. Rainforest does. A missed fraud event is our problem, not yours.

Card data never touches your infrastructure. Merchants onboard through your interface while the payment infrastructure runs behind the scenes. Your team streamlines operations without building internal compliance workflows.

And because Rainforest only earns when your merchants process, the partnership runs more like a proactive payments department than a passive vendor. Skin in the game on adoption, volume, and retention. Not just signature.

How much of the payments stack you actually want to own

There are three ways to structure your payments program, each defined by how much of the operational stack you take on. Becoming a PayFac (short for payment facilitator) means running the whole thing yourself. PayFac-as-a-Service gives you PayFac-level economics without the compliance and risk lift. An referral model is the lightest touch, but you give up most of the merchant relationship.

Here's how they compare:

Becoming a PayFac

- Highest control and margin potential

- Often 100+ basis points in margin, but requires large up-front investment and high operating costs

- You own compliance, reserves, underwriting, and fraud liability

- Might make sense for platforms processing multiple billions annually with experience in-house fintech, risk, and compliance teams, but many platforms scale to billions without ever becoming a registered PayFac

Partnering with a PayFac-as-a-Service provider

- Combines favorable economics with lower operational burden

- Your payments partner handles compliance and risk

- You own merchant relationships, pricing, and data

- Typical launch timeline: weeks instead of 12–18 months

- Best for most vertical SaaS platforms

Using a referral model

- Lowest initial lift

- Lowest margin

- Limited merchant ownership and control over the overall merchant experience

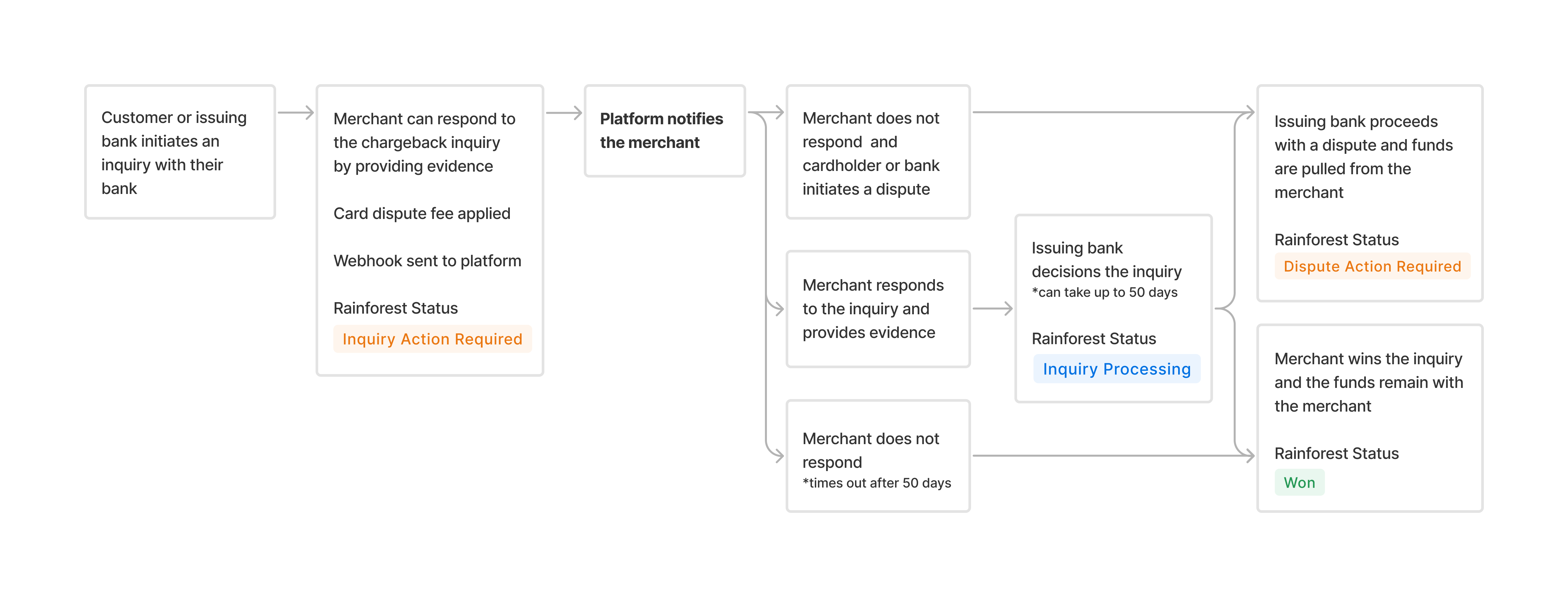

Disputes, chargebacks, and deposit strategy as a product lever

Disputes and chargebacks are more than a support cost. They hit merchant retention, drag on your support team, and drag down your long-term monetization economics.

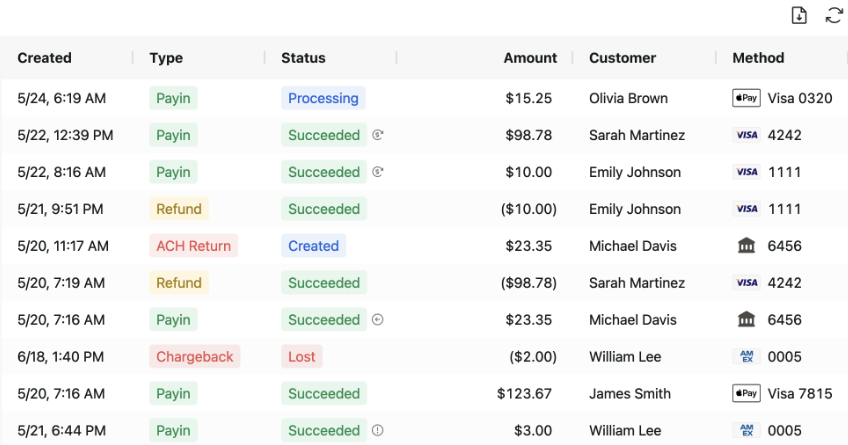

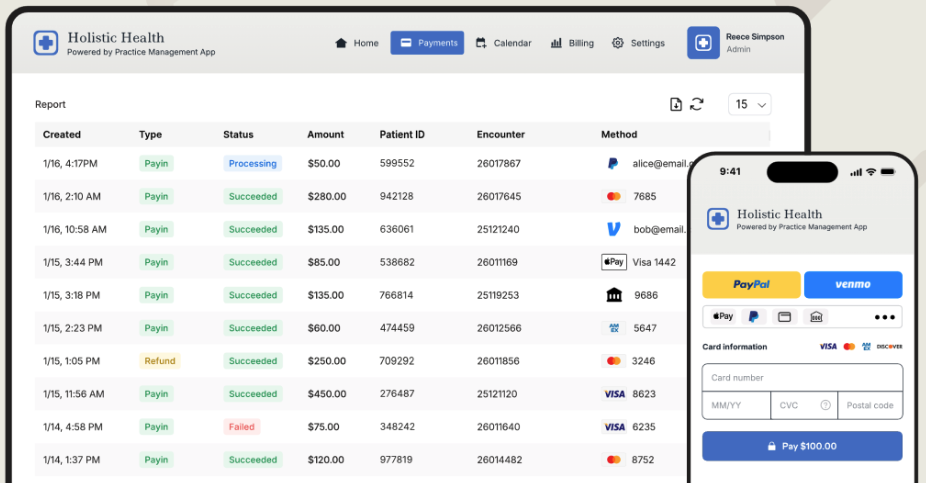

That's because merchants judge you on how disputes feel. Real-time visibility, fast evidence submission, clear status updates. That's the bar. When disputes live in a separate portal, you lose control of the relationship and add friction to everyday workflows. Deposits work the same way. Timely deposits are a feature merchants actively shop for, and building them into your pricing models turns speed into a revenue lever.

Rainforest’s embedded chargeback management component makes it easy for merchants to respond to chargebacks, and for platforms to guide merchants through the process or respond on their behalf. Platforms get full visibility into dispute data and deposit configuration.

And when merchants have questions, they’ll receive direct support from the platform team they know and trust. Rainforest empowers platforms to support their merchants, while providing tier 2 support with a team of real humans who know your vertical and your business, not a generic escalation queue. Platforms are often surprised to find that support load decreases when they move from a referral model to Rainforest, because their team is equipped to quickly resolve the vast majority of requests without escalating to the payment provider.

How to measure payment monetization success in your first 180 days

Four metrics tell you whether your embedded payments program is growing revenue or just creating operational friction. Track them from day one.

Attach rate is the percentage of new customers signing up for payments. It's a read on your marketing, your sales process, and your onboarding flow, and how well all three drive payments adoption at the point of signup. Maximize attach rates from day 1. Every customer who doesn’t sign up for payments when they onboard becomes a backbook adoption challenge later.

Adoption rate is the percentage of eligible customers using payments. It tells you how broadly the product has spread across your existing customer base. A platform with 1,000 customers and a 50% adoption rate has 500 on payments. The other 500 are your opportunity.

Net payments revenue is what's left after interchange (paid to the issuing banks), dues, fees, and assessments (paid to the card networks), and buy rate (paid to the payment processor).

Take-rate tells you how much you’re actually earning on your processing volume. Calculate it by dividing your residual or net revenue by total payment volume. If you earned $50k on $10M payment volume, your take rate is 50 basis points.

At Rainforest, our tech is purpose-built for vertical SaaS platforms ready to process more volume at higher margins. We handle onboarding, KYC, fraud protection, compliance, and chargebacks, so your team focuses on adoption, retention, and growth.

Frequently asked questions about monetizing payments for SaaS platforms

How do SaaS companies actually make money from embedded payments?

SaaS companies make money from embedded payments by keeping a share of the processing revenue on every transaction. Your payments partner charges you a buy rate, you charge merchants a higher retail rate, and your platform keeps the spread. The result is a recurring revenue stream tied directly to how much your merchants process.

What is a good take rate for a vertical SaaS payments program?

The definition of a good take rate depends on your payments leadership structure, vertical, and the sophistication of your payments program. Higher rates mean more revenue, while lower rates might boost adoption and retention – to a point. Many platforms tier pricing by merchant size, so larger merchants pay lower rates and smaller merchants pay higher rates.

When should a vertical SaaS platform consider becoming a PayFac?

Becoming a registered PayFac sounds wonderful, but in reality, the costs of becoming a PayFac can very rapidly consume most of the payments revenue. In fact, operating as a PayFac can be 10x the cost of working with an embedded payments provider.

For most vertical SaaS platforms, working with a PayFac-as-a-Service provider is the better call. It gets you to launch in a minimum of weeks instead of month to years. It also keeps the operational lift low, without giving up the economics that make payments monetization worth doing.

Share this article

Subscribe to our blog

Be the first to hear about new content

Related articles

View all articles

.png)

Get started today.

Boost revenue with Rainforest

Get Started

Legal

© 2026 Rainforest Pay, Inc